May 16, 2026

Roth Conversion Strategy for Early Retirees: How ACA Subsidies Change the Math

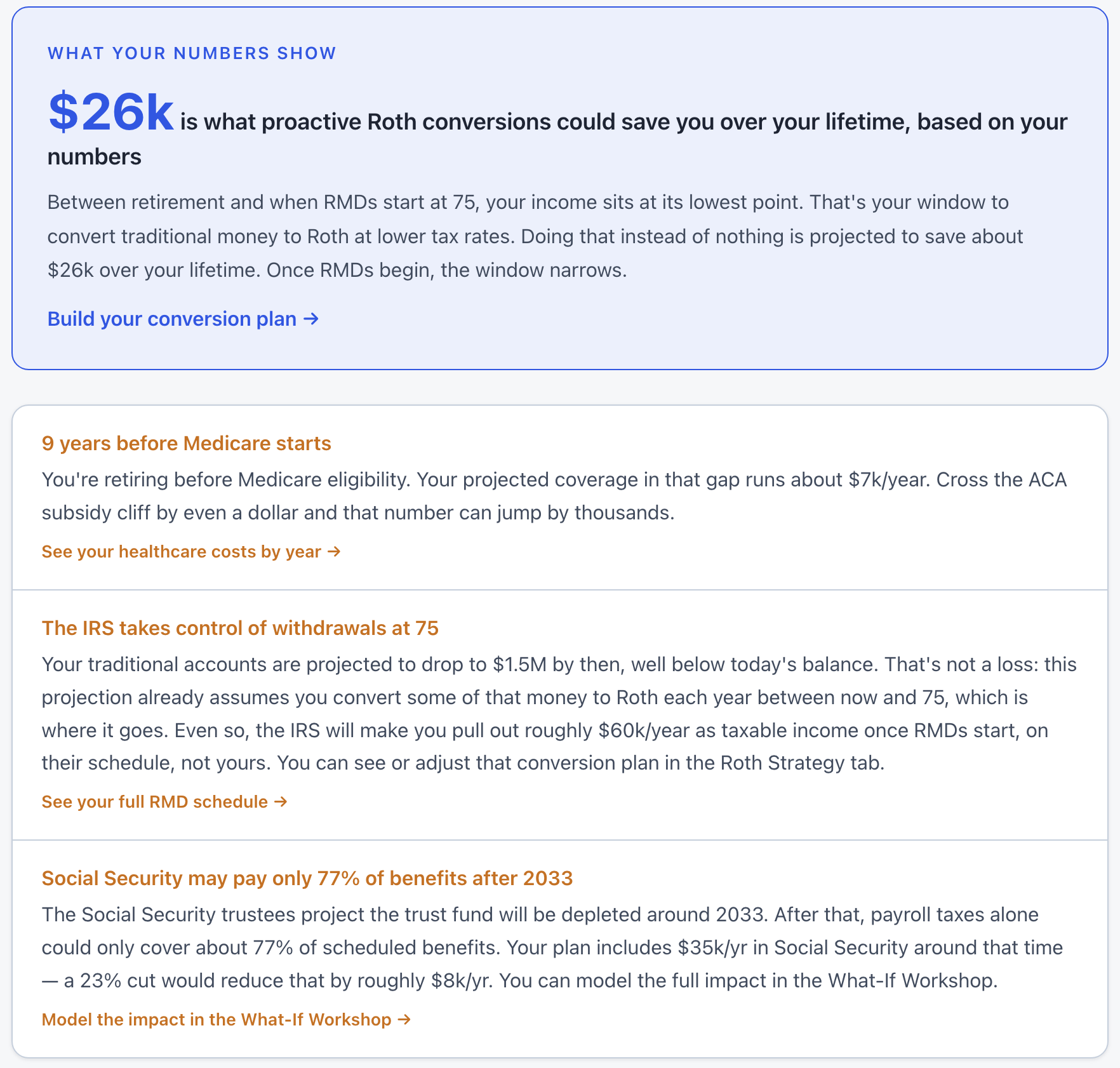

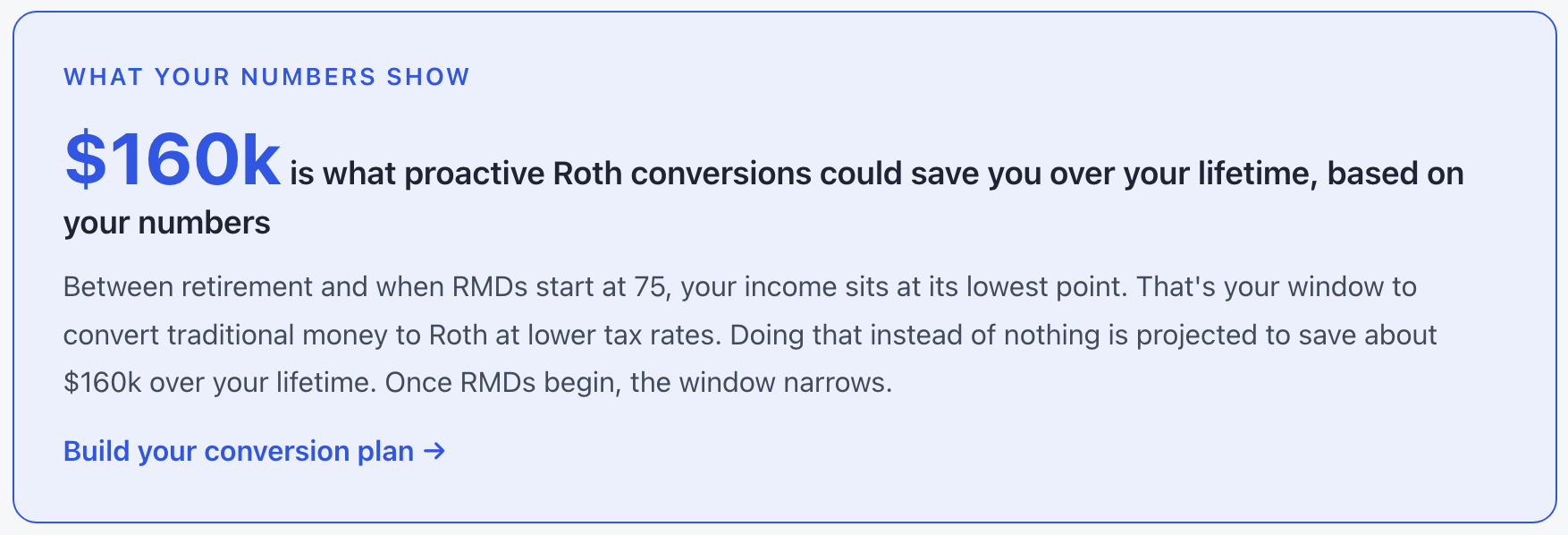

If you are planning to retire before age 65, you have probably already heard the standard advice about Roth conversions. You move money from a traditional IRA or 401k into a Roth account, pay taxes now at today’s rates, and reduce excess forced income later when required minimum distributions start at age 73 or 75 (depending on your birth year), specifically the portion that would exceed your inflation-adjusted spending at that age. Most retirement calculators tell you to convert as much as you can each year, especially in the gap between when you stop working and when Social Security or RMDs kick in. The logic is sound, and for someone retiring at 65 it is mostly correct. For someone retiring at 55 or 60, the story is more complicated, and the part that gets left out of most articles can quietly cost you tens of thousands of dollars.

Why Roth Conversions Are More Expensive Before You Turn 65

Between the day you retire and the day you turn 65, you need health insurance from somewhere. COBRA covers you for 18 months at most, after which you are on your own. Most early retirees end up on an ACA marketplace plan. These plans are not cheap on their own. For someone in their late fifties or early sixties, the full unsubsidized premium for a Silver plan can easily run $900 to $1,400 per month, or somewhere between $10,000 and $17,000 per year. For a couple, double that.

The reason most people don’t pay anywhere near that amount is the premium tax credit, which subsidizes ACA coverage based on your household income. The lower your income, the bigger the subsidy. The higher your income, the smaller the subsidy. At certain income levels, the subsidy disappears entirely.

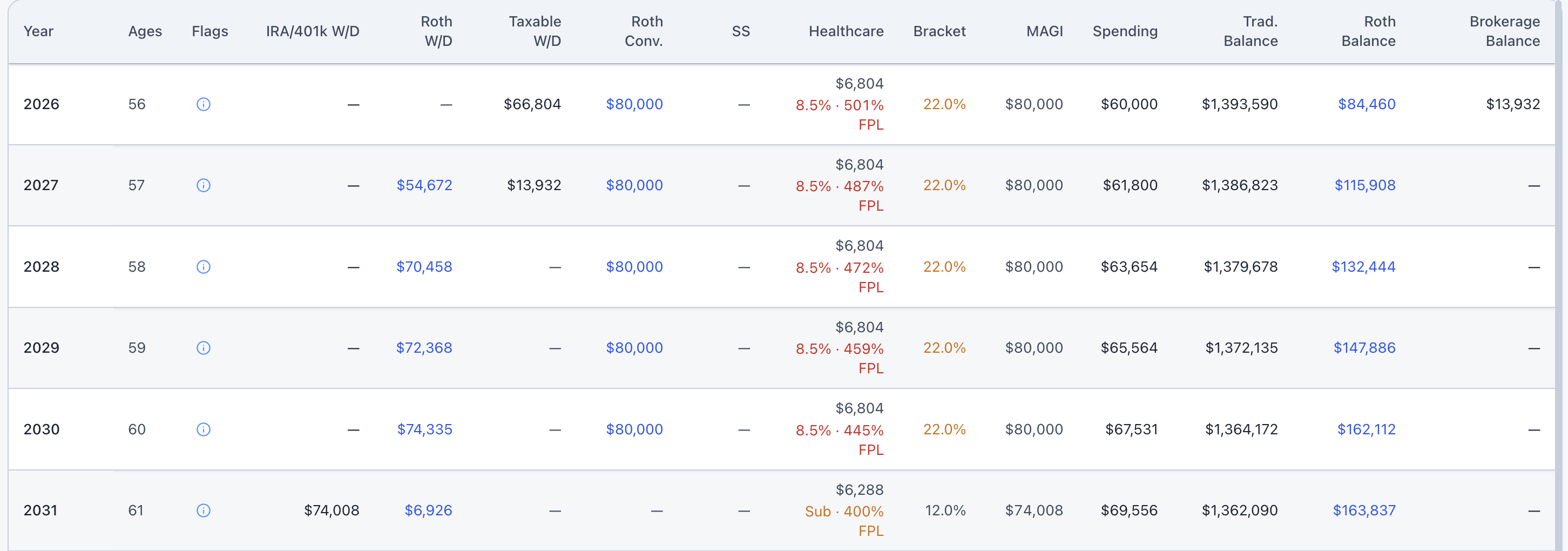

This is where Roth conversions enter the picture, because converting traditional money to a Roth shows up as ordinary income on your tax return. The IRS sees you taking $40,000 out of your traditional IRA the same way it sees you earning $40,000 from a job, even though you are really just moving the money into a different retirement account. That income counts toward the figure the ACA uses to decide your subsidy, called MAGI, or modified adjusted gross income.

So the moment you start converting, your reported income goes up, and your ACA subsidy goes down. If you convert aggressively, you can wipe out your subsidy entirely. That is a cost that almost no traditional Roth conversion calculator includes, and it is a real expense that gets paid every month in higher health insurance premiums.

How ACA Premium Subsidies Are Calculated for Retirees

To make this concrete, the ACA looks at your household income as a percentage of the federal poverty level for your household size. A single retiree with $40,000 of income is at roughly 255 percent of FPL. A couple with $60,000 is at roughly 285 percent. The subsidy is calculated so that you never pay more than a certain percentage of your income toward the benchmark Silver plan in your area. At lower income levels, that capped percentage is small. At higher income levels, it grows.

From 2021 through 2025, an enhanced subsidy rule capped your premium contribution at 8.5 percent of household income no matter how high your income climbed, with no cutoff at all. That enhancement expired at the end of 2025 and Congress did not renew it. Under the original rules now back in effect, the required percentage climbs to roughly 10 percent of income at 400 percent of the federal poverty level, and above that line the subsidy disappears entirely. More income means a smaller subsidy, and past the 400 percent line it means no subsidy at all. The size of that swing can easily be five to fifteen thousand dollars a year per person, and for a couple it can be more.

That number is what makes the standard early retirement Roth conversion strategy fall apart if you ignore it.

Case Study: How an $80,000 Roth Conversion Cost One Retiree $73,000 in Lost Subsidies

Consider Maria, age 56, who retires with $1.4 million in a traditional 401k and $80,000 in a taxable brokerage account. She has no Roth money yet. Her plan is to live on her brokerage account for the first few years, supplemented by Roth conversions to build up her future tax free bucket and avoid massive RMDs at 73.

Maria runs the numbers and decides to convert $80,000 per year from her traditional IRA to a Roth IRA. She figures she will stay in the 22 percent federal tax bracket, well below where she was while working, and she is right. Her federal tax bill on the conversion is about $11,000. That part of the plan works as expected.

What Maria didn’t model is what that $80,000 conversion does to her ACA subsidy. Living off only brokerage withdrawals, her MAGI would be around $20,000, mostly from dividends. At that income level she qualifies for a substantial subsidy, and the Silver plan in her county costs her about $80 per month, or roughly $1,000 per year.

Add the $80,000 conversion to her MAGI and she jumps to $100,000 of income. Her subsidy mostly evaporates. The same Silver plan now costs her about $760 per month, or $9,100 per year.

The conversion saved her future RMD taxes, but it just cost her $8,100 a year in higher health insurance premiums. Multiply that by the nine years until she is eligible for Medicare and that single decision costs her roughly $73,000 in lost subsidies, on top of the federal taxes she is already paying on the conversion itself.

The future tax savings from the conversion are also real. Avoiding a 24 percent or higher tax rate in her seventies on the same dollars is worth something. But once you net the ACA penalty against the RMD tax savings, the conversion that looked obviously good on a traditional retirement calculator now looks much closer to break even, and depending on how she invests the Roth money, it might actually be a net loss.

When Smaller Roth Conversions Still Make Sense in the Bridge Years

The right takeaway is not that early retirees should skip Roth conversions entirely. It is that the size of the conversion needs to be calibrated against the subsidy you are giving up.

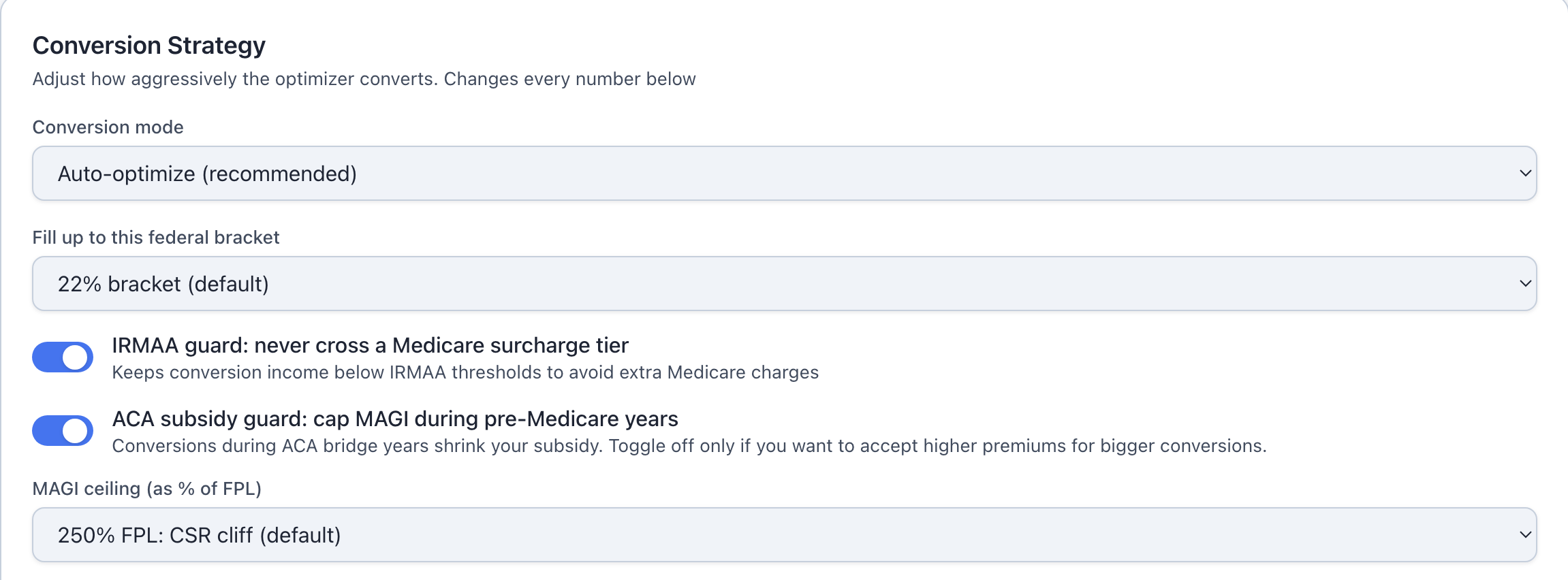

Smaller conversions, on the order of $20,000 to $40,000 a year, often still come out ahead. Below 400 percent of the federal poverty level, ACA subsidies taper off gradually as your income rises, they do not disappear suddenly. A modest conversion might cost you a thousand or two in lost subsidy while saving you significantly more in future RMD taxes. The trade off gets ugly fast if the conversion is large enough to push you past 400 percent of FPL, where the entire subsidy disappears at once rather than continuing to taper.

There is also the timing question. A conversion you do in year one of retirement, when you have nine years of ACA exposure left, costs you a lot of subsidy years. A conversion you do in year eight, when you only have one ACA year left to worry about, barely costs anything in subsidy terms. So one practical strategy is to keep conversions small or zero in the early bridge years, and then ramp them up as your remaining ACA years dwindle and you approach Medicare eligibility. Our full Roth conversion strategy guide walks through the year by year framework in more detail.

Case Study: A Couple Five Years From Medicare

Consider David and Susan, both 60, retiring together with $2 million split mostly across traditional accounts and a small Roth. Their plan is to bridge to Social Security at 67 and Medicare at 65, using a mix of brokerage and Roth withdrawals to keep their reported income low.

Without any Roth conversions, their MAGI lands around $35,000 for a few years. As a couple at roughly 165 percent of FPL, their ACA subsidy is significant. The benchmark Silver plan for the two of them in their area costs them around $115 per month combined after subsidy.

Now consider what happens if they convert $60,000 per year. Their MAGI climbs to $95,000, well above the 400 percent FPL cliff for a couple, around $84,000. Their subsidy does not just shrink. It disappears completely. Their net Silver plan cost jumps from $115 per month to the full unsubsidized rate, roughly $2,200 per month for two 60-year-olds. That is an increase of about $25,000 a year in health insurance cost, every year they continue converting at that level.

But David and Susan have something Maria doesn’t. They are only five years out from Medicare. After they both turn 65, ACA exposure ends and they can convert aggressively without any health insurance impact. So a smarter version of their plan would be smaller conversions in the bridge years, maybe $20,000 to $30,000 between them, and much larger ones from 65 to 73.

When their numbers are run through a planner that models both effects together, the optimal conversion path saves them roughly $40,000 over their full retirement compared to either converting nothing or converting as much as possible.

Case Study: When Aggressive Conversions Still Work in Early Retirement

There is also a case where the standard advice still works, and it is worth covering because not every early retiree should be conservative.

Take Ryan, 50, who retired early with $2.5 million and has 15 years before Medicare. His income comes from a paid off rental property that throws off $40,000 a year, which means his MAGI is already comfortably above the meaningful ACA subsidy range no matter what else he does. The subsidy ship has already sailed for him. He pays close to full price for ACA coverage regardless of whether he converts.

For Ryan, doing aggressive Roth conversions early actually makes sense, because the ACA cost is fixed and the RMD avoidance benefit is huge over a 23 year accumulation window in his Roth. The trap that catches Maria and the Andersons doesn’t apply to him at all.

The lesson here is not “don’t convert” but “model both effects against your specific situation before deciding.” There is no universal right answer. There is only the right answer for your specific income, your specific account balances, and your specific number of bridge years.

Why Roth Conversions Get Easier After Age 65

Once you turn 65 and move to Medicare, ACA stops mattering for your healthcare costs. But a different income test takes over, called IRMAA, which adds surcharges to your Medicare Part B and Part D premiums when your income crosses certain thresholds. The math is similar in spirit. Big conversions can cost you, but IRMAA surcharges are much smaller in absolute dollars than ACA subsidy losses. We are talking a few hundred to a few thousand dollars per year, not five figures.

What this means in practice is that your post 65 years are a much better window for aggressive Roth conversions than your bridge years. You have roughly eight years between Medicare eligibility and the start of RMDs at 73, and during most of those years you can convert tens or even hundreds of thousands of dollars while incurring only modest IRMAA penalties. This is where the big tax bracket arbitrage happens for most retirees, and it is where most of the conversion volume should land if you are optimizing across your full retirement.

The order matters too. Money converted at 65 has eight years to grow tax free before RMDs would have started touching it. Money converted at 56 has even longer, of course, but only if the cost of doing the conversion at 56 doesn’t exceed the cost of waiting until 65. For most people, that math comes out in favor of waiting. If you want to understand the mechanics of how forced withdrawals build up over time, our piece on the 401k RMD bomb is a good companion read.

Building a Roth Conversion Plan That Accounts for Health Insurance

If you are planning to retire before 65 and you have been told you should max out Roth conversions in your gap years, get a second opinion that includes ACA modeling. The advice is technically correct from a pure tax perspective, but it leaves out the healthcare cost side of the ledger, which for someone in their late fifties can be the bigger number.

What you actually want is an integrated plan that looks at federal tax cost, ACA subsidy cost, IRMAA exposure, and future RMD tax exposure all together, and finds the conversion schedule that minimizes the total cost across your whole retirement, not just one of those four numbers in isolation. In practice, that optimal plan almost always involves smaller conversions in the bridge years, possibly zero in some years, followed by much larger conversions from 65 to 72. The exact shape depends on your specific income, your specific account balances, your state, and which year of your bridge you are in.

This is one of the things ThunderHarbor was built to do. The planner models all of these effects together, including the ACA subsidy interaction that most calculators ignore. The What If Workshop lets you try out different conversion amounts in different years and see what happens to your total retirement cost, not just your tax bill. The result is often surprising even for people who thought they had a good handle on the trade off.

The general rule, if you want one sentence to take away from all of this, is this. Roth conversions are a great long term strategy, but the years between your retirement date and Medicare eligibility are the worst window to do them aggressively, and the years between Medicare and RMDs are the best.

Plan accordingly, and you can save yourself a five figure mistake that most people never see coming.

Not financial advice

This article is for informational purposes only. Nothing here constitutes financial, tax, or legal advice. ACA subsidy rules and tax brackets change from year to year. Always consult a qualified professional before making significant financial decisions.

See your own Roth conversion sweet spot

ThunderHarbor models ACA subsidies, IRMAA surcharges, and RMD taxes together so you can find the conversion schedule that minimizes your total retirement cost.

Start your free plan