Roth Conversion Strategy: A Practical Guide

A Roth conversion moves money from a traditional IRA or 401(k) into a Roth account. You pay income tax on the converted amount today, but all future growth and withdrawals are tax-free. Done strategically across the right years, this can save hundreds of thousands of dollars in lifetime taxes.

What a Roth conversion actually does

When you convert, the IRS treats the converted amount as ordinary income in that calendar year. If you convert $50,000, your taxable income rises by $50,000. You owe whatever bracket rate applies to that amount, and then the money is done being taxed forever. It grows tax-free in the Roth account, and you never have to take required minimum distributions from it during your lifetime.

The reason conversions matter is that traditional retirement accounts carry a deferred tax liability. Every dollar sitting in a pretax 401(k) or IRA will eventually be taxed as ordinary income, either when you withdraw it voluntarily or when the IRS forces you to withdraw it through required minimum distributions starting at age 72, 73, or 75 (depending on your birth year, under SECURE Act 2.0). Converting before that happens gives you control over when and at what rate that tax is paid.

The conversion window

The ideal time to convert is the stretch of years between when you retire and when required minimum distributions begin (age 72, 73, or 75 depending on your birth year). During this window your taxable income is often at its lowest point in decades. You may have no earned income yet, Social Security may not have started, and you are not yet being forced to take withdrawals. That combination creates unusually wide room in the lower tax brackets.

The goal is to fill a bracket each year without spilling into the next one. A married couple filing jointly in 2026 can have up to approximately $94,300 in taxable income and stay in the 12% bracket. If their other income that year is $30,000, they can convert up to $64,300 at just 12%, a rate many people will never see again once RMDs and Social Security stack together later in retirement.

Bracket fill scenarios (married filing jointly, 2026)

The table below shows how much a married couple can convert while staying entirely within the 12% bracket, depending on what other taxable income they already have that year. The standard deduction is already accounted for in these figures.

| Other taxable income | 12% space remaining | Max conversion at 12% | Tax owed on conversion |

|---|---|---|---|

| $15,000 | $79,300 | $79,300 | $9,516 |

| $30,000 | $64,300 | $64,300 | $7,716 |

| $50,000 | $44,300 | $44,300 | $5,316 |

| $75,000 | $19,300 | $19,300 | $2,316 |

Tax owed = conversion amount × 12%. The 12% bracket for MFJ runs from $23,200 to $94,300 in taxable income (2026). Figures assume no other income sources beyond what is listed.

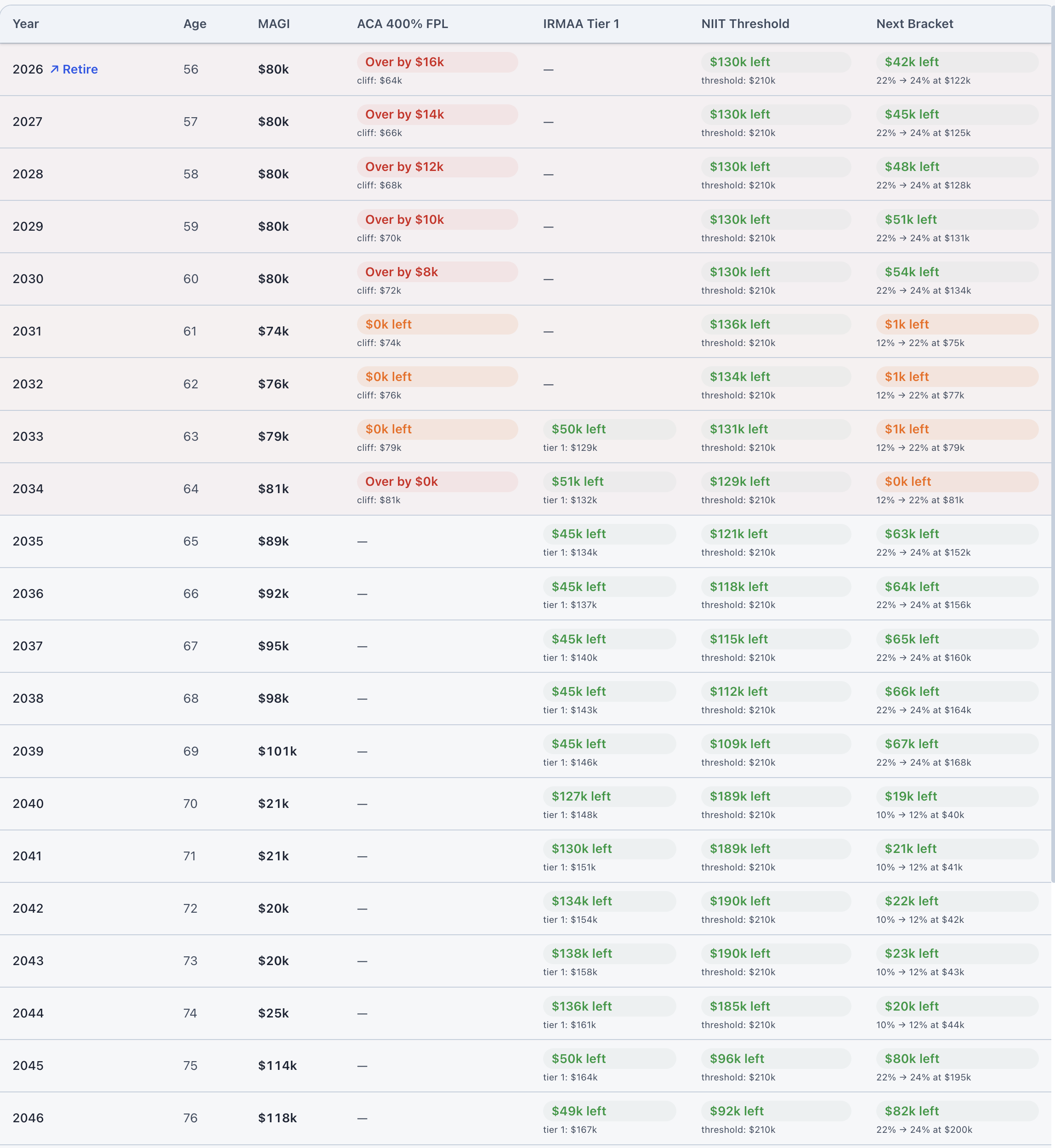

IRMAA and the two-year lookback

If you are on Medicare or approaching it, Roth conversions have a hidden cost that most people miss. Medicare Part B and D premiums are based on your modified adjusted gross income from two years prior. This is called IRMAA, the Income-Related Monthly Adjustment Amount. For 2026, a married couple with MAGI above $212,000 starts paying higher premiums. At the top tier, the surcharge can reach over $600 per person per month on top of the standard premium.

The two-year lookback means a conversion you do today can raise your Medicare bill two years from now. A large conversion at age 63 hits you at age 65 when Medicare begins. This does not mean you should avoid conversions near Medicare age, but it does mean you need to model the IRMAA cost alongside the tax savings, and sometimes spreading conversions across more years at lower amounts produces a better net result than doing one large conversion in a single year.

Watching the tax cliffs

A Roth conversion raises your income, which means it can push you across thresholds that cost far more than the tax on the conversion itself. The ACA subsidy cliff is one example: if you are on marketplace health insurance before Medicare, crossing 400% of the Federal Poverty Level can wipe out thousands of dollars in annual subsidies with a single dollar of extra income. IRMAA tiers are another. The Net Investment Income Tax kicks in above $250,000 for married couples. And bracket edges can mean that the marginal dollar of conversion is taxed at an effective rate much higher than the stated bracket rate.

ThunderHarbor's Tax Cliffs tab shows your income projected against all four of these thresholds simultaneously, year by year, so you can see in real time whether a conversion amount you are considering stays safely below the danger zones or crosses one.

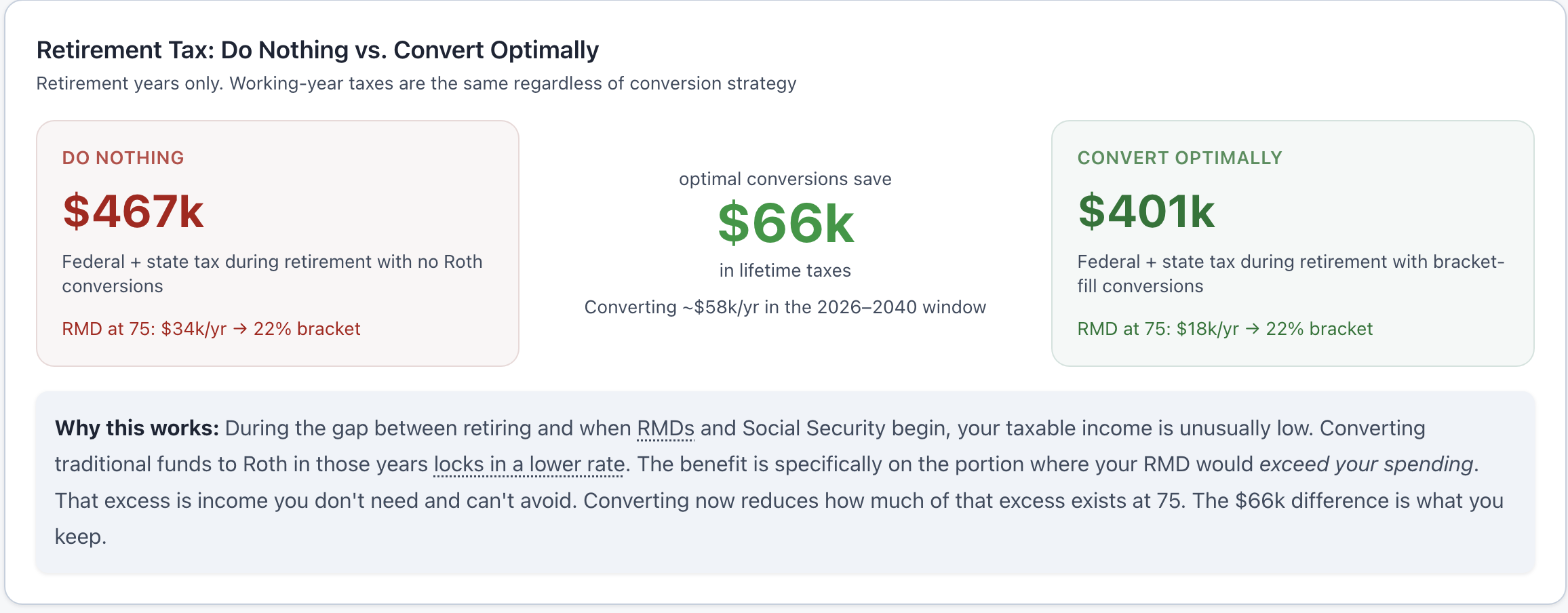

The mistakes that cost people the most

The most common and expensive mistake is converting too much in a single year. A large conversion that pushes you into the 32% bracket or triggers a higher IRMAA tier can cost more in taxes and premiums than years of Roth growth will recover. The fix is straightforward: spread conversions across multiple years and stay within a defined bracket ceiling each time.

Ignoring state taxes is another overlooked error. Several states treat Roth conversions as ordinary income. If you plan to move to a state with no income tax during retirement, converting before the move can mean paying a state tax bill that you would have avoided entirely by waiting.

People also sometimes convert when their traditional balance is too small for it to matter. If your pretax savings are modest, RMDs may generate very little forced income, and there is limited benefit to paying tax now to convert money that would have been taxed lightly anyway. The five-year rule matters too: converted amounts must stay in the Roth account for five years or until age 59½, whichever is later, before the earnings can be withdrawn penalty-free. Converting late in life or very close to when you need the money can trip this rule.

The underlying issue with all of these mistakes is the same: the optimal conversion amount is specific to your balances, income sources, state, timeline, and Medicare situation. No rule of thumb covers it. ThunderHarbor's Roth Strategy tab runs the full year-by-year calculation with your actual numbers, showing you the conversion amount that fills your bracket without triggering IRMAA or other cliffs.

Not financial advice

This guide is for informational purposes only. Nothing here constitutes financial, tax, or legal advice. Always consult a qualified professional before making significant financial decisions.

Find your optimal conversion amount

ThunderHarbor's Roth Strategy tab calculates the optimal conversion for each year, accounting for brackets, IRMAA, ACA cliffs, state taxes, and your full retirement timeline.

Build your free planFree plan included · Full Roth optimizer with Premium ($47/year)