May 9, 2026

How to Defuse the 401k RMD Bomb & Avoid Taxes

We have all heard the golden rule of personal finance since our twenties: start saving early. Time is the market’s greatest lever, and the math is undeniably beautiful. If you diligently stash away money in a tax-deferred 401k for forty years, compounding interest will do the heavy lifting for you. By the time you are ready to hang it up and enjoy your retirement around age sixty-seven, those decades of contributions will have likely grown into a 7-figure nest egg. It feels like you have completely won the game. But what most people do not realize is that for certain savers, specifically those whose forced distributions will exceed what they actually need to spend, this success comes with a tax planning challenge that is worth understanding early.

You’re not avoiding taxes. You’re delaying them.

When you put money into a traditional 401k, you are not actually avoiding taxes. You are simply delaying them. The government is allowing your money to grow untouched for decades, but their patience runs out exactly when you turn 73. That is the age when RMDs (Required Minimum Distributions) kick in. The IRS steps in and mandates that you start withdrawing a percentage of your tax-deferred accounts every single year. The amount is calculated from your balance, not from your spending needs. When your balance has grown large enough that the forced withdrawal significantly exceeds what you planned to spend, the difference is taxable income you did not choose to take, and that gap is what this article is really about.

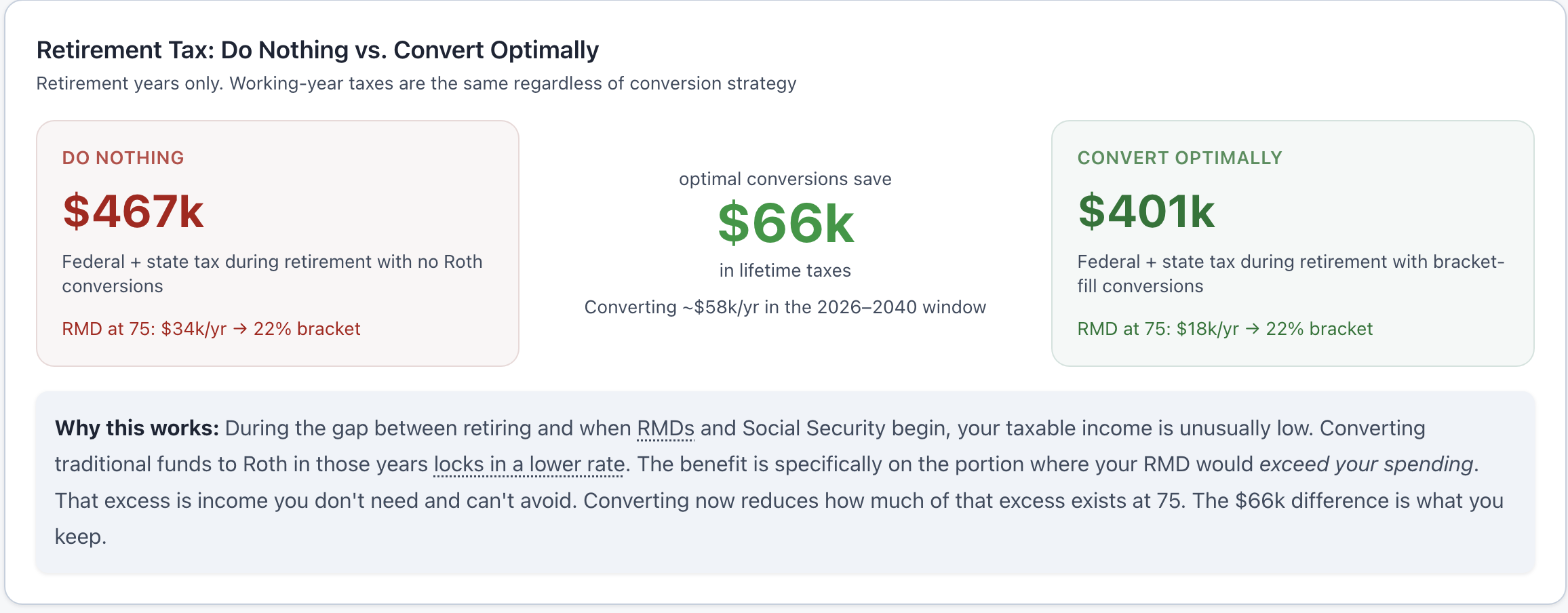

The six-year window

If you retire at 67 and RMDs start at 73 (or 75 if born in 1960 or later), you have a window where you control your own taxable income. Once RMDs begin, the withdrawal amount is set by the IRS formula, not by what you need. If your balance has grown large, those withdrawals could significantly exceed your inflation-adjusted spending. That excess is the real problem: taxable income you do not need, stacking on top of Social Security and any other income you have.

The domino effect

The excess forced income stacks on top of pension and Social Security. For people with large traditional balances and modest spending needs, this can push their effective tax bracket higher than it was during their working years, not because they are spending more, but because they are forced to take income they do not need. That is the core problem the planning conversation should be about: the gap between your forced withdrawal and your actual spending.

But the higher tax bracket is only the beginning of the problem. The hidden gut-punch is how this artificial income spike affects your healthcare. Medicare premiums are tied directly to your income through something called the IRMAA surcharge. When your forced retirement distributions spike your taxable income, your Medicare costs skyrocket right along with it. Between the elevated tax brackets and the inflated healthcare premiums, you can easily end up handing over significantly more money to the government in your seventies than you ever did in your forties.

Why the old advice breaks down

The old advice assumed that retiring means your income drops. For moderate savers that is still true, and for them traditional 401k contributions remain a great deal: defer taxes at a high rate while working, pay them at a lower rate in retirement. The advice breaks down for people whose portfolio has grown large enough that forced withdrawals will significantly exceed their inflation-adjusted spending. At that point the deferral advantage disappears, and the planning question becomes how to eliminate the excess, not whether the traditional account was the right choice.

Why Roth changes everything

This is exactly why understanding the difference between traditional and Roth accounts is so critical. The choice between the two is not just a minor administrative detail; it is the entire foundation of your future tax burden. While traditional contributions give you a small tax deduction today, you are essentially going into a lifelong business partnership with the IRS, and you have absolutely no idea what tax rates they will decide to charge you when it is time to cash out.

Roth accounts change the dynamic entirely. You pay the tax upfront at today’s known rates. After that, the money grows completely tax-free, and more importantly, it comes out completely tax-free. There are no forced withdrawals at age seventy-three. There are no sudden artificial income spikes that trigger massive Medicare surcharges. Every single dollar sitting in a Roth account is a dollar that belongs entirely to you.

Obviously, the math depends on your specific situation, your company match, and your current tax bracket. But for anyone who has the massive advantage of time on their side, taking the tax hit today is very often the cheapest price you will ever pay.

The goal isn’t the number on the screen

The ultimate goal of retirement planning should never just be about hitting a big number on a screen. It should be about making sure you get to keep as much of that number as possible when you finally need it most.

That is why I am building ThunderHarbor. It runs the year-by-year math on your actual accounts: balances, tax brackets, IRMAA thresholds, and Social Security. It shows you exactly how to optimize your strategy before the window closes. No rules of thumb, no generic advice. Just the numbers for your specific situation.

Not financial advice

This article is for informational purposes only. Nothing here constitutes financial, tax, or legal advice. Always consult a qualified professional before making significant financial decisions.

See your RMD bomb and how to defuse it

ThunderHarbor projects your RMDs, brackets, and IRMAA surcharges year by year, and calculates the optimal strategy to minimize lifetime taxes.

Start your free plan