May 13, 2026 · Updated May 16, 2026

Pretax vs Roth in Your 40s: Why the Standard Advice Gets It Wrong

If you are in your forties and you have a 401k, you have almost certainly been told to keep your contributions pretax. The conventional pitch is that you are in your peak earning years, so it makes sense to defer the tax bite until you are retired and in a lower bracket. This is the default advice from most financial advisors, most online calculators, and most of your friends who watch finance YouTube. It is also wrong for a large group of people, and for a smaller group it is dangerously wrong. The frustrating part is that the right answer for you depends on numbers that most generic advice never asks about. To show what I mean, let me walk through three case studies that show when Roth wins, when pretax still wins, and the trap that catches a surprising number of high earners in their forties.

How Marginal Tax Brackets Actually Work for Married Couples

Before the case studies, one concept needs to be straight, because almost all bad pretax vs Roth advice comes from confusing average tax rate with marginal tax rate.

Your marginal rate is the rate that applies to your next dollar of income. When you make a 401k contribution, the tax savings happen at your marginal rate, not your overall effective rate. For married couples filing jointly in 2026, taxable income from roughly $24,000 to $97,000 sits in the 12 percent bracket. From $97,000 to $207,000 it is the 22 percent bracket. Above that you are in 24 percent and higher.

The key word there is taxable income, which is what you have left after the standard deduction (about $32,000 for married filing jointly in 2026), traditional 401k contributions, HSA contributions, and a handful of other items. So a couple earning $135,000 gross, contributing $24,000 to a traditional 401k, and using the standard deduction has taxable income of about $79,000, which puts them firmly in the 12 percent bracket. That is the number that matters for the Roth question, not the $135,000 you see on your W2.

Almost everybody underestimates how low their actual marginal bracket is when they have a non working spouse or one income earner doing most of the heavy lifting. Many couples who think they are “in the 22 percent bracket” because that is what their paychecks suggest are actually paying 12 percent on the marginal dollar once you do the full calculation.

Case Study: A Single Income Family in the 12 Percent Bracket

Consider Maria and David. Maria is 42 and earns $130,000 as a project manager. David stays home with their two kids. They have $450,000 saved across her traditional 401k and a rollover IRA, all of it from Maria’s contributions over the last 18 years. She contributes $24,000 a year to her 401k pretax.

When Maria sits down with a generic retirement calculator, it tells her to keep doing exactly what she is doing. Pretax contributions reduce her current tax bill, she will be in a lower bracket in retirement, classic textbook advice.

Here is what the textbook advice misses. Maria and David’s taxable income after her pretax contributions and the standard deduction is roughly $74,000. That is in the 12 percent federal bracket with comfortable headroom. Maria is not paying 22 percent on her contributions today. She is paying 12 percent.

Now project forward. Maria plans to retire at 65, which gives that $450,000 traditional balance 23 more years to grow. Add 23 years of $24,000 annual contributions on top. At a 7 percent return, by the time she is 65 she has roughly $3.2 million in traditional accounts. By the time RMDs start at 73 or 75, that balance has grown to about $5.5 million if she has not started drawing it down.

The first year RMD on $5.5 million is approximately $208,000. Add two Social Security checks for Maria and David, even modestly assumed, and they are looking at $265,000 of taxable income, forced, every year, with no ability to opt out. That puts them in the 24 percent federal bracket, possibly the 32 percent bracket depending on what tax law looks like in 2057.

So Maria’s choice today is this. Keep contributing pretax and save 12 cents in tax on every dollar she puts in. Or switch to Roth, pay 12 cents in tax today, and never pay tax again on the same dollar or its growth, even when she is 80 and forced to take it out.

The math is not even close. She is buying tax free growth at a 12 percent discount when she would otherwise pay 24 percent or more on the same dollars in retirement. Over 23 years of contributions and 30 plus years of retirement withdrawals, the cumulative difference for Maria’s family is in the high six figures. Switching her contributions to Roth today saves them roughly $480,000 in lifetime taxes compared to continuing pretax, under reasonable assumptions about future rates.

The standard advice gave Maria the wrong answer. Not because the advice was wrong in principle, but because the advice was generic and her situation is specific.

Case Study: When Pretax Is Still the Better Choice

Now consider Priya and Vikram, both 44, both engineers, both earning $185,000 each. Combined gross income $370,000. They have $300,000 in traditional accounts and contribute the max to both their 401ks.

For them, the math goes the other way. Their taxable income after the standard deduction and pretax contributions is about $290,000. They are paying 24 percent at the margin on every additional dollar of income, and a small slice is even in the 32 percent bracket.

If they switch to Roth, that 24 percent marginal rate applies to the entire $46,000 they contribute, instead of being deferred. They are sending the IRS an extra $11,000 every year, today, that they could otherwise have invested.

The question becomes whether their retirement marginal rate will be higher than 24 percent. For a household this high earning, the answer is probably no, even with sizable RMDs. By the time their accounts mature, they will be drawing maybe $300,000 to $400,000 per year of total income. The top of that lands in the 24 percent bracket today, and even if rates rise modestly, they are probably still in the 22 to 24 percent range when they retire.

For Priya and Vikram, pretax is the right call. They are paying a higher marginal rate today than they will face in retirement on the same dollars. The standard advice works for them precisely because their bracket is high enough that future relief is likely.

The lesson is not “Roth always wins” or “pretax always wins.” It is that the bracket arbitrage works in the direction of whatever bracket you are currently in, compared to your expected retirement bracket. Low bracket now and a likely higher bracket later means Roth. High bracket now and a likely lower bracket later means pretax. The trap is when you assume the second case applies to you when really the first one does.

Case Study: The Hidden RMD Trap for High Earners in Their 40s

There is a third case worth telling because it shows the most expensive version of getting this wrong.

Mark is 46 and earns $215,000 as a marketing director. His wife Karen is 45 and earns $80,000 as a teacher. Combined gross $295,000. They are diligent savers, maxing Mark’s 401k plus the employer match plus Karen’s contributions. They have $720,000 in traditional accounts and zero Roth.

On the surface this looks like the Priya and Vikram case. They are clearly in a 24 percent bracket on the margin. Pretax should be the right answer. And for the current contribution decision, they are mostly right that pretax saves them more today than Roth would.

But here is what the simple comparison misses. Mark and Karen are 20 years from retirement. Their current $720,000 plus 20 more years of $30,000 annual combined contributions, growing at 7 percent, becomes $4.1 million by retirement. After 8 more years of growth before RMDs, it is approaching $7 million.

The first year RMD on $7 million is about $264,000. That alone puts them in the 24 percent bracket. Add two Social Security checks, maybe a pension, maybe some part time income, and they are well into the 32 percent bracket on the margin, with IRMAA Medicare surcharges adding another four to six thousand dollars a year per person on top.

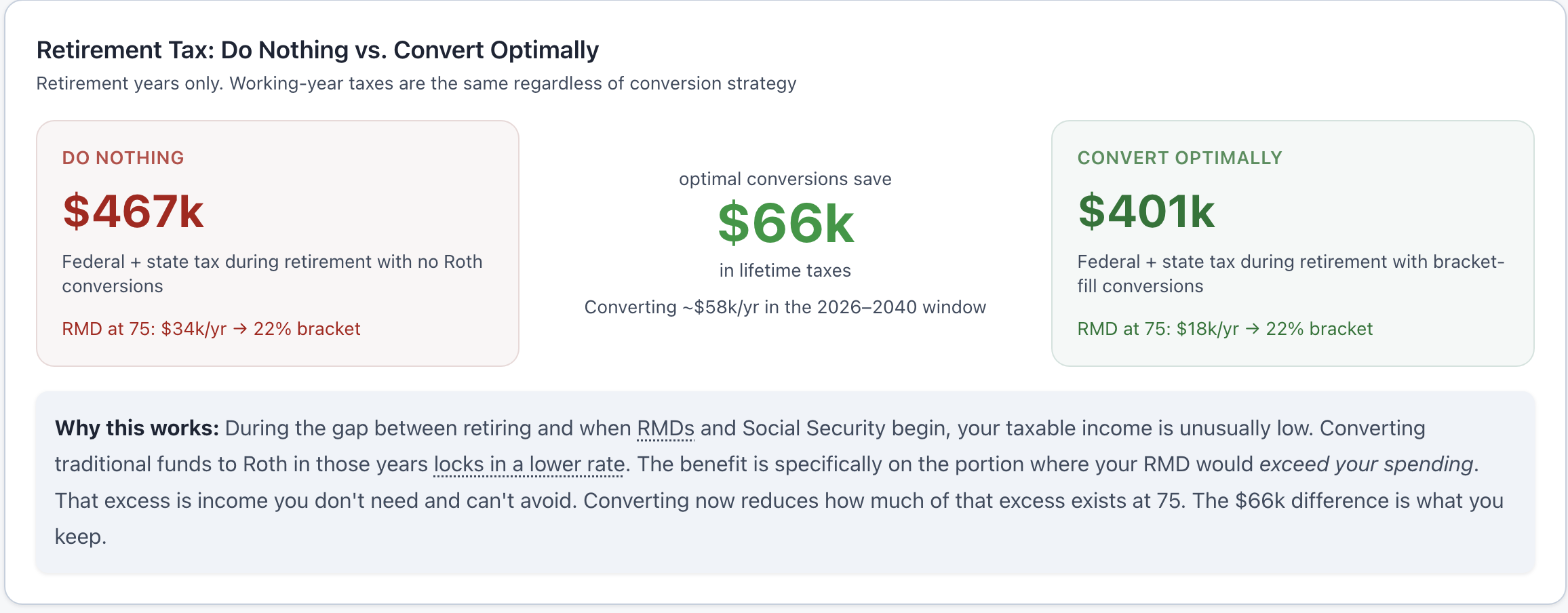

So Mark and Karen’s current pretax decisions are saving them 24 percent today, but their RMDs at 73 are projected to significantly exceed their inflation-adjusted spending. That excess forced income will likely be taxed at 24 to 32 percent. The deferral is not moving them to a lower bracket. It is keeping them in the same bracket on income they do not need, while adding IRMAA on top and removing all flexibility about when income hits.

The right move for Mark and Karen is mixed. The current pretax contributions are fine for now, but they need a serious Roth conversion strategy in their fifties and early sixties to draw down that traditional balance before RMDs force the issue. If they ignore the conversion question and just keep stacking pretax, they will end up with a tax bill in their seventies that completely surprises them. (Our full piece on the 401k RMD bomb walks through how this builds.)

This is the case that catches a lot of high income forties households. They are in the right bracket today to do pretax. But they are accumulating so aggressively that their retirement bracket will be just as high, and they will lose the option to manage it. The fix is not necessarily switching contributions to Roth right now. It is being aware that the accumulation creates a future problem that needs an active plan, not a passive default.

What to Actually Do With Your Next 401k Contribution

The honest answer is that the right contribution mix depends on five inputs nobody likes to gather. Your current marginal federal bracket. Your current marginal state bracket. The expected size of your traditional balance at age 73. Your expected Social Security and pension income. And your willingness to do Roth conversions in the gap years between retirement and 73.

A useful shortcut, if you do not want to model all of that yourself, is this. If your taxable income puts you in the 12 percent federal bracket, lean heavily toward Roth, possibly all Roth. If you are in the 22 percent bracket, the answer is genuinely a mix and depends on your other accounts. If you are in the 24 percent bracket or higher and you already have a sizable traditional balance, default to pretax now but commit to a Roth conversion plan starting the year you retire. If you are in the 24 percent bracket or higher but your traditional balance is still small, lean Roth, because you are at the beginning of accumulating and you have more time to compound tax free.

The bigger mistake than picking the wrong account type is picking it once and forgetting. Even if you start with the wrong mix at 42, revisiting it at 47 and again at 52 catches most of the damage. The decision changes as your income changes, as your accounts grow, as your retirement timeline shortens. Plan to make this decision more than once.

The general rule, if you want one sentence, is this. Pretax wins when your current bracket is higher than your retirement bracket. Roth wins when it is lower or the same. And for many middle income households with a non working spouse or one dominant earner, the current bracket is much lower than it feels, which is why so many people pick pretax when Roth would have been the better deal.

ThunderHarbor’s planner does this whole calculation for you. You plug in your actual income, your actual balances, your actual retirement age, and it shows you the year by year tax cost of each path, including the RMD trap that none of the simple calculators catch. The answer is often the opposite of what you expected, and the opposite of what your generic 401k provider told you.

Not financial advice

This article is for informational purposes only. Nothing here constitutes financial, tax, or legal advice. Tax brackets and contribution limits change from year to year. Always consult a qualified professional before making significant financial decisions.

See the actual pretax vs Roth math for your situation

ThunderHarbor models both paths with your real income, balances, and retirement timeline, including the RMD bracket trap that simple calculators miss.

Start your free plan