Understanding Required Minimum Distributions (RMDs)

If you have money in a traditional 401(k) or IRA, the IRS will eventually force you to withdraw it and pay tax on it. These required withdrawals are called Required Minimum Distributions, and they start at age 72, 73, or 75 depending on your birth year (SECURE Act 2.0). Understanding how they work is one of the most important things you can do before retirement.

Why the IRS requires them

When you contributed to a traditional 401(k) or IRA, you got a tax deduction. The IRS did not forgive that tax permanently. They deferred it. RMDs are the collection mechanism. Your RMD start age depends on your birth year: 72 if you were born in 1950 or earlier, 73 if you were born between 1951 and 1959, and 75 if you were born in 1960 or later. Starting that year, you must withdraw a minimum amount from your traditional accounts each year regardless of whether you need the income. The withdrawn amount is taxed as ordinary income, just like a paycheck. You can always withdraw more than the minimum, but never less without facing a penalty.

Roth accounts work differently. A Roth IRA has no RMDs during the original owner's lifetime. A Roth 401(k) technically did have RMDs under old rules, but SECURE Act 2.0 eliminated that requirement starting in 2024. This means every dollar you move into Roth before RMDs begin is a dollar that will never generate a forced taxable withdrawal.

How the calculation works

Your RMD each year is your account balance on December 31 of the prior year divided by a life expectancy factor from the IRS Uniform Lifetime Table. At 73, that factor is 26.5, meaning you withdraw roughly 3.8% of your balance. The percentage rises every year as the factor shrinks. By age 85 you are withdrawing over 6% annually; by age 90, over 8%. These withdrawals add to your income on top of Social Security and any other sources whether you want them or not.

RMD amounts by age and balance

The table below shows annual RMD amounts across different ages and account balances, calculated using the IRS Uniform Lifetime Table. A couple with $1 million in traditional accounts will be forced to take roughly $75,000 per year at their RMD start age combined, even if their actual spending is lower.

| Age | IRS Factor | RMD on $500k | RMD on $1M | RMD on $2M |

|---|---|---|---|---|

| 73 | 26.5 | $18,868 | $37,736 | $75,472 |

| 75 | 24.6 | $20,325 | $40,650 | $81,301 |

| 80 | 20.2 | $24,752 | $49,505 | $99,010 |

| 85 | 16.0 | $31,250 | $62,500 | $125,000 |

| 90 | 12.2 | $40,984 | $81,967 | $163,934 |

| 95 | 9.6 | $52,083 | $104,167 | $208,333 |

RMD = prior year-end balance ÷ IRS Uniform Lifetime Table factor. Factors from the 2022 IRS update (effective for 2023 and beyond). Balances shown are illustrative starting amounts; actual balances change with growth and withdrawals each year.

Why large RMDs create a tax problem

RMDs stack on top of your other income. If you are receiving Social Security, that already generates taxable income. Then RMDs push you further up the brackets, possibly into a higher rate than your actual spending ever required. For a married couple where each spouse has $800,000 in traditional accounts, combined RMDs starting at their RMD age could easily exceed $60,000 per year, all of it ordinary income, all of it taxed at whatever bracket applies.

The IRMAA impact compounds this further. Because Medicare premiums are based on your income from two years earlier, large RMDs raise your Medicare costs two years later. Surcharges can add $200 to $600 per person per month that most people never anticipated when they were saving. ThunderHarbor's RMD Analyzer shows exactly how your forced withdrawals grow each year from your RMD start age to 95 and how they interact with your tax bracket and IRMAA tier simultaneously.

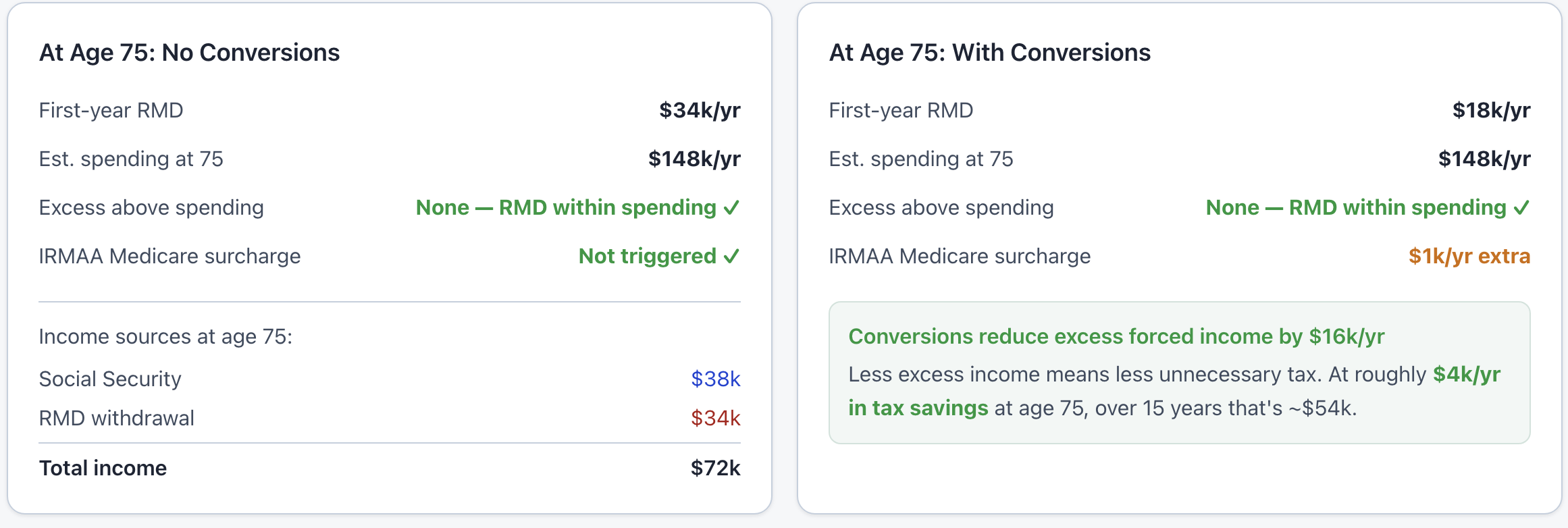

Strategies that reduce RMDs

Roth conversions before RMDs begin are the most powerful tool available. Every dollar you convert to Roth before RMDs begin is a dollar that will never generate a forced taxable withdrawal. The years between retirement and your RMD start age (72, 73, or 75 depending on your birth year) are the conversion window, often a period of unusually low income where conversions can be done at 12% or 22%, far below the bracket rate those RMDs might otherwise have triggered later.

Qualified Charitable Distributions offer another option once you reach age 70½. You can direct up to $108,000 per year directly from your IRA to a qualified charity, and that distribution satisfies your RMD without being counted as taxable income. If you are charitably inclined anyway, a QCD is almost always better than withdrawing the money, paying tax on it, and then donating after-tax dollars.

Spending from traditional accounts earlier in retirement, before RMDs begin, is also effective. Drawing down the pretax balance reduces the future RMD. The math is simple: a smaller balance at RMD start means smaller forced withdrawals. If you have both Roth and traditional accounts available in your 60s, drawing from traditional first while letting Roth continue to grow tax-free can meaningfully reduce the RMD burden in your 70s and 80s.

For anyone with a SEPP arrangement or early retirement before age 59½, the SEPP Planner in ThunderHarbor models how those penalty-free withdrawals interact with your future RMD trajectory and ACA exposure simultaneously.

What happens to an inherited IRA

If you leave a traditional IRA to a non-spouse beneficiary, they cannot stretch withdrawals over their own lifetime the way they could before the SECURE Act. Under current rules, most beneficiaries must empty the inherited account within 10 years of your death. That means they absorb the full balance as ordinary income over a decade, potentially at the highest tax rates of their peak earning years. A $500,000 traditional IRA inherited by a child in their 40s or 50s can generate a six-figure tax bill that Roth conversions during your lifetime could have largely prevented. ThunderHarbor's Inherited IRA Analyzer shows the year-by-year depletion schedule and estimated tax cost so you can see what your heirs would actually keep.

Penalties for missing an RMD

Under SECURE Act 2.0, the penalty for failing to take an RMD is 25% of the shortfall, reduced from the previous 50%. If you correct the mistake within two years by taking the missed distribution and filing IRS Form 5329, the penalty drops to 10%. The IRS has historically been willing to waive penalties for reasonable cause on a first offense, but the process requires a written explanation and is not automatic.

Not financial advice

This guide is for informational purposes only. Nothing here constitutes financial, tax, or legal advice. Always consult a qualified professional before making significant financial decisions.

See your RMD projections to age 95

ThunderHarbor's RMD Analyzer shows forced withdrawal amounts year by year alongside your tax bracket and IRMAA tier, so you can see the full cost of inaction.

Build your free planFree plan included · RMD Analyzer + Inherited IRA with Premium ($47/year)