The Social Security Tax Torpedo: How It Works and How to Avoid It

Most retirees assume their Social Security benefit is either tax-free or taxed at their regular rate. In reality, one extra dollar of income, an RMD, a Roth conversion, even interest from a CD, can simultaneously make a chunk of your Social Security taxable for the first time. The combined effect is often called the tax torpedo, and it can push your effective marginal rate on that single dollar well above your nominal bracket.

What the tax torpedo actually is

Up to 85% of your Social Security benefit can be subject to federal income tax, but only if your other income crosses certain thresholds. Below those thresholds, your benefit is entirely tax-free. The "torpedo" is what happens at the crossing point: as your other income rises through the threshold zone, each additional dollar does double duty, it is taxed itself, and it drags a portion of your previously tax-free Social Security benefit into taxable territory along with it.

The result is a stretch of income, often spanning tens of thousands of dollars, where your effective marginal tax rate is meaningfully higher than your stated bracket. A household in the 22% bracket can find that the next dollar of ordinary income actually costs them 30 to 40 cents once the Social Security effect is included.

How much of your benefit gets taxed

The IRS determines the taxable portion using a figure called "combined income": your adjusted gross income, plus any tax-exempt interest, plus half of your Social Security benefit. Where that number lands relative to the thresholds below determines how much of your benefit becomes taxable.

| Filing status | Combined income | Taxable portion |

|---|---|---|

| Single | Below $25,000 | 0% taxable |

| Single | $25,000 – $34,000 | Up to 50% taxable |

| Single | Above $34,000 | Up to 85% taxable |

| Married filing jointly | Below $32,000 | 0% taxable |

| Married filing jointly | $32,000 – $44,000 | Up to 50% taxable |

| Married filing jointly | Above $44,000 | Up to 85% taxable |

These thresholds were set in the 1980s and 1990s and are not adjusted for inflation. Every year, more retirees cross them simply because incomes and balances have grown.

Why one extra dollar can cost you 40 cents

Picture a married couple with combined income sitting right at $40,000, already inside the 50%-to-85% phase-in zone. Their next dollar of ordinary income, say from an IRA withdrawal, is taxed at their regular bracket. But that same dollar also raises their combined income, which can convert up to 85 cents of additional Social Security benefit from tax-free to taxable. Now two things are being taxed from one dollar of decisions, and the effective rate on that dollar can run 1.5 to 1.85 times the nominal bracket rate.

This is not a one-time event. It persists across the entire phase-in range, which can span $9,000 to $12,000 of combined income depending on filing status. Anyone whose income sits inside that band for multiple years is paying the elevated rate year after year, often without realizing why their tax bill looks larger than their bracket would suggest.

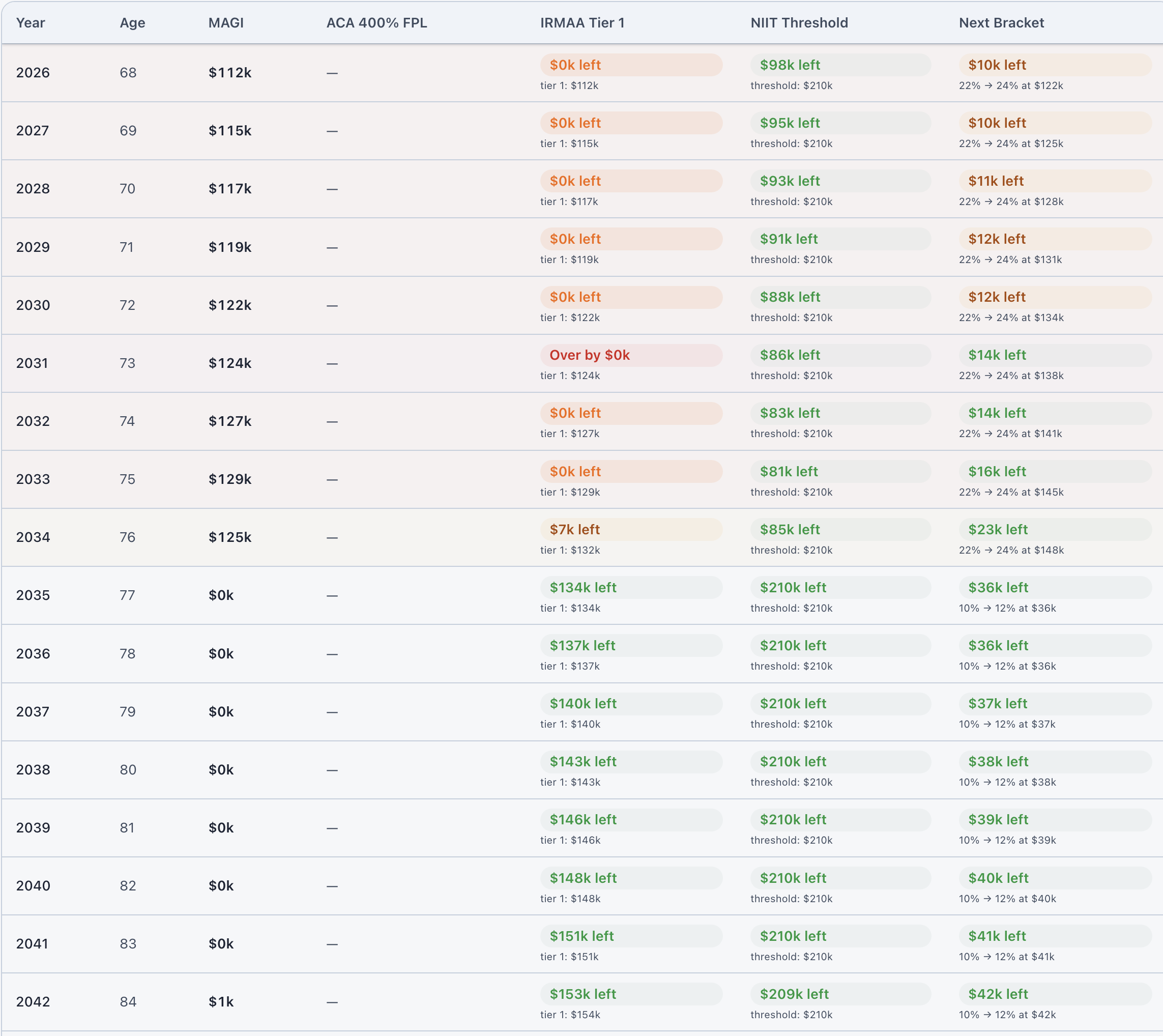

How RMDs and Roth conversions trigger the torpedo

Required minimum distributions are one of the most common triggers, because they are forced and grow larger every year you delay them. A retiree who comfortably avoided the torpedo in their late 60s can find themselves squarely inside it once RMDs begin at their RMD start age (72, 73, or 75 depending on birth year), simply because the forced withdrawal raised their adjusted gross income.

Roth conversions create the same effect in the years you do them. A conversion that looks attractive on paper, because it fills a low bracket, can quietly cost more than expected if it also pushes a chunk of your Social Security into taxable territory for that year. That does not necessarily mean you should avoid the conversion, often it is still the right move long-term, but it does mean the true cost needs to include the Social Security effect, not just the conversion's own tax bill.

Strategies that reduce the torpedo's bite

The most effective tool is sequencing: doing the bulk of your Roth conversions in the years before you claim Social Security, when there is no benefit yet to drag into taxable territory. This is one more reason the gap between retirement and your claiming age, and the gap before RMDs begin, is so valuable for tax planning.

Once benefits have started, drawing from Roth or taxable brokerage accounts in years where ordinary income would otherwise cross a threshold can keep you out of the phase-in zone. Holding municipal bonds is not necessarily a clean fix either, since tax-exempt interest still counts toward combined income. The only reliable way to manage this is to project your full income picture, including future RMDs, several years ahead and choose which accounts to draw from accordingly.

Not financial advice

This guide is for informational purposes only. Nothing here constitutes financial, tax, or legal advice. Always consult a qualified professional before making significant financial decisions.

See exactly when the torpedo hits your plan

ThunderHarbor projects your combined income year by year, so you can see precisely when your Social Security becomes taxable and how RMDs and conversions change that picture.

Build your free planFree plan included · Full tax projections with Premium ($47/year)