Retirement Withdrawal Strategies: Which Accounts to Tap First

The order you withdraw from retirement accounts can save or cost hundreds of thousands of dollars in taxes over a 30-year retirement. The same $1,000,000 portfolio produces dramatically different after-tax outcomes depending on which accounts you draw from, in what sequence, and how that sequence interacts with Social Security, RMDs, and Medicare premiums.

Why withdrawal order matters

Different account types are taxed differently: traditional 401(k) and IRA withdrawals are taxed as ordinary income, Roth withdrawals are tax-free, and taxable brokerage accounts generate capital gains when you sell. When you withdraw from each type determines your taxable income each year, which determines your tax bracket, which determines how much of your money you actually keep.

The stakes are highest in the years between retirement and your RMD start age (72, 73, or 75 depending on your birth year), when required minimum distributions begin. During that window your income is often at its lowest point in decades: no earned income, possibly no Social Security yet, and no forced withdrawals. These are the years when you have the most control over your taxable income, and the decisions you make in them ripple through every year that follows.

The three account types

Tax-deferred (Traditional 401k, Traditional IRA)

Taxed as ordinary income on withdrawal. Contributions were tax-deductible. Growth is tax-deferred. Required minimum distributions begin at age 72, 73, or 75 depending on your birth year (SECURE Act 2.0).

Tax-free (Roth 401k, Roth IRA)

No tax on qualified withdrawals. Contributions were made after-tax. Growth is tax-free. No RMDs for the original owner during their lifetime.

Taxable (Brokerage account)

Capital gains tax when you sell. Long-term gains are taxed at 0%, 15%, or 20% depending on income. Tax-loss harvesting can offset gains. No forced withdrawals.

The conventional withdrawal order

The standard advice for withdrawal sequencing is: taxable accounts first, then tax-deferred traditional accounts, then tax-free Roth last. The logic is that tax-advantaged accounts should be allowed to continue growing as long as possible. Roth accounts, which have no RMDs and grow forever tax-free, should be the last thing you touch.

This conventional order works well in simple scenarios. But real retirement rarely follows a simple pattern, and blindly following the conventional order can cost significantly more in taxes than a deliberate bracket-aware strategy.

When the conventional order backfires

The most common case where conventional sequencing fails is when you have large traditional account balances approaching RMD age. If you hold $800,000 in a traditional IRA and defer all withdrawals until RMDs begin, the IRS will force you to take roughly $30,000 per year starting at your RMD age, rising to over $50,000 per year by 80, stacked on top of Social Security and any other income. Drawing down the traditional balance in your 60s, before RMDs arrive, often produces a much lower lifetime tax bill even if it means touching the account sooner.

A related situation is the Roth conversion window. In the years between retirement and RMD onset, your income is often low enough that you can convert traditional assets to Roth at 12% or 22%, rates that may be unavailable later when Social Security and RMDs stack together. Doing Roth conversions during this window is effectively a form of strategic withdrawal from the traditional account, even though you are not spending the money. Skipping this window to preserve the traditional balance, as conventional advice suggests, can lock you into higher brackets for the rest of your retirement.

IRMAA thresholds create another exception. Medicare Part B and D premiums are based on your income from two years prior, so a large withdrawal from a traditional account in a given year can raise your Medicare costs two years later. If your income is near an IRMAA tier boundary, drawing from Roth or taxable accounts in that year instead of traditional, even if conventional logic says otherwise, can prevent a surcharge worth hundreds of dollars per month.

The 0% long-term capital gains bracket is the fourth exception most people overlook. For 2026, married couples filing jointly pay 0% on long-term gains as long as taxable income stays below approximately $94,050. In a low-income year where you are drawing primarily from Roth accounts or living on Social Security, you may have room to realize taxable gains at no cost, harvesting appreciation that would otherwise be taxed later at 15% or 20%.

Withdrawal sequencing by retirement phase

The right withdrawal source shifts depending on which phase of retirement you are in. The table below shows how the optimal approach changes as Social Security, Medicare, and RMDs enter the picture.

| Phase | Primary source | Strategic priority |

|---|---|---|

| Early retirement, pre-SS (60–67) | Taxable brokerage | Fill the 12–22% bracket with Roth conversions from traditional accounts while income is low |

| Medicare starts, pre-RMD (65–73) | Taxable or Roth | Watch the 2-year IRMAA lookback; keep MAGI below tier 1 ($212k MFJ) to avoid $100+/month surcharges |

| Social Security started, pre-RMD (67–73) | Taxable; traditional for bracket fill | SS now partially taxable; limit additional traditional withdrawals to avoid 85% SS inclusion threshold |

| RMDs mandatory (73+) | RMDs are unavoidable | Use Roth for discretionary spending above RMD; consider Qualified Charitable Distributions to satisfy RMD without taxable income |

Phases overlap and vary by individual. Social Security and RMD onset depend on your claiming and birth year. IRMAA tiers and capital gains thresholds are 2026 figures for married filing jointly.

The bucket strategy

Some retirees use a bucket approach to manage withdrawals across different time horizons. The idea is to keep near-term spending in stable assets so you are never forced to sell growth investments during a market downturn.

Short-term (1–2 years)

Cash, money market, short-term bonds. Covers near-term spending regardless of market conditions. Refilled from other buckets periodically.

Medium-term (3–10 years)

Bonds, dividend stocks, balanced funds. Generates income and moderate growth. Replenishes Bucket 1 when markets cooperate.

Long-term (10+ years)

Growth stocks, equity funds. Left alone to grow through market cycles. Sells to refill Bucket 2 during good years.

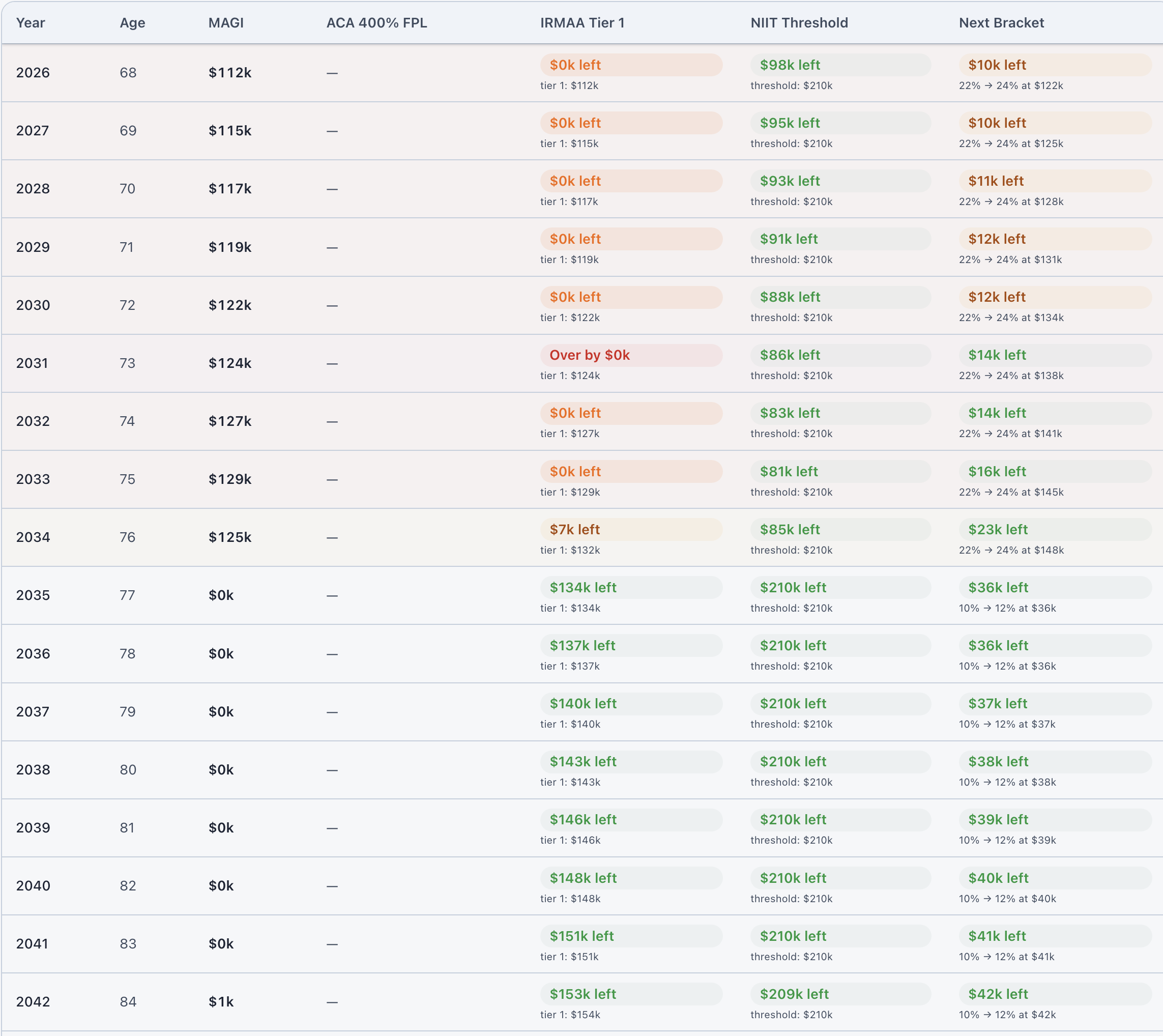

The bucket strategy is primarily a behavioral tool. It keeps you from selling equity during a downturn by giving you a pool of safe assets to draw from first. For tax optimization, you still need to decide which account types fund each bucket and in what order withdrawals happen across them. ThunderHarbor's Projection Table and What-If Workshop let you model exactly how different sequences play out year by year with your actual balances.

Coordinating with Social Security and RMDs

Your withdrawal strategy needs to account for the income streams already coming your way. Social Security adds to taxable income. Up to 85% of your benefit becomes taxable once combined income crosses $44,000 for married couples. RMDs stack on top of that once they begin at your RMD age (72, 73, or 75 depending on your birth year). Once both are running, your brackets may already be largely filled before you take a single discretionary withdrawal.

The years before these streams begin are the most strategically valuable years in retirement. Once Social Security and RMDs are active, much of your income is determined for you, and your flexibility to manage brackets narrows significantly. Decisions made in the early retirement years. Decisions such as whether to convert, which accounts to spend from, and how much to realize in capital gains shape the tax environment for the decades that follow. ThunderHarbor's Tax Cliffs tab shows your projected income against every relevant threshold year by year, so you can see the consequences of each sequencing choice before you make it.

Not financial advice

This guide is for informational purposes only. Nothing here constitutes financial, tax, or legal advice. Always consult a qualified professional before making significant financial decisions.

Model the optimal withdrawal order for your accounts

ThunderHarbor's Projection Table and What-If Workshop model withdrawal sequencing across all your accounts, factoring in taxes, RMDs, Social Security, and IRMAA, to minimize lifetime taxes over your full retirement.

Build your free planFree plan included · Full projection and scenario modeling with Premium ($47/year)