Pretax vs Roth 401(k): Which Is Better for You

The standard advice is to compare your current tax rate against your expected rate in retirement. That comparison is directionally correct, but it misses enough nuance to lead people toward the wrong choice with real money. The actual decision depends on your bracket today, how large your pretax balance already is, what state you will retire in, and how aggressively you plan to convert before required minimum distributions begin.

How pretax 401(k) contributions work

Pretax contributions reduce your taxable income today. If you earn $120,000 and contribute $20,000 pretax, your W-2 shows $100,000. You pay tax on $100,000 instead of $120,000. The money grows tax-deferred, and you pay ordinary income tax when you withdraw it in retirement.

Your employer match is always pretax even if you contribute Roth, so you will always have some pretax balance growing regardless of which contribution type you choose.

How Roth 401(k) contributions work

Roth contributions are made with after-tax dollars. Your paycheck is taxed as if you contributed nothing, so $120,000 in income means $120,000 on your W-2. But the money grows tax-free and comes out tax-free in retirement. There is no income tax on growth and no income tax on qualified withdrawals.

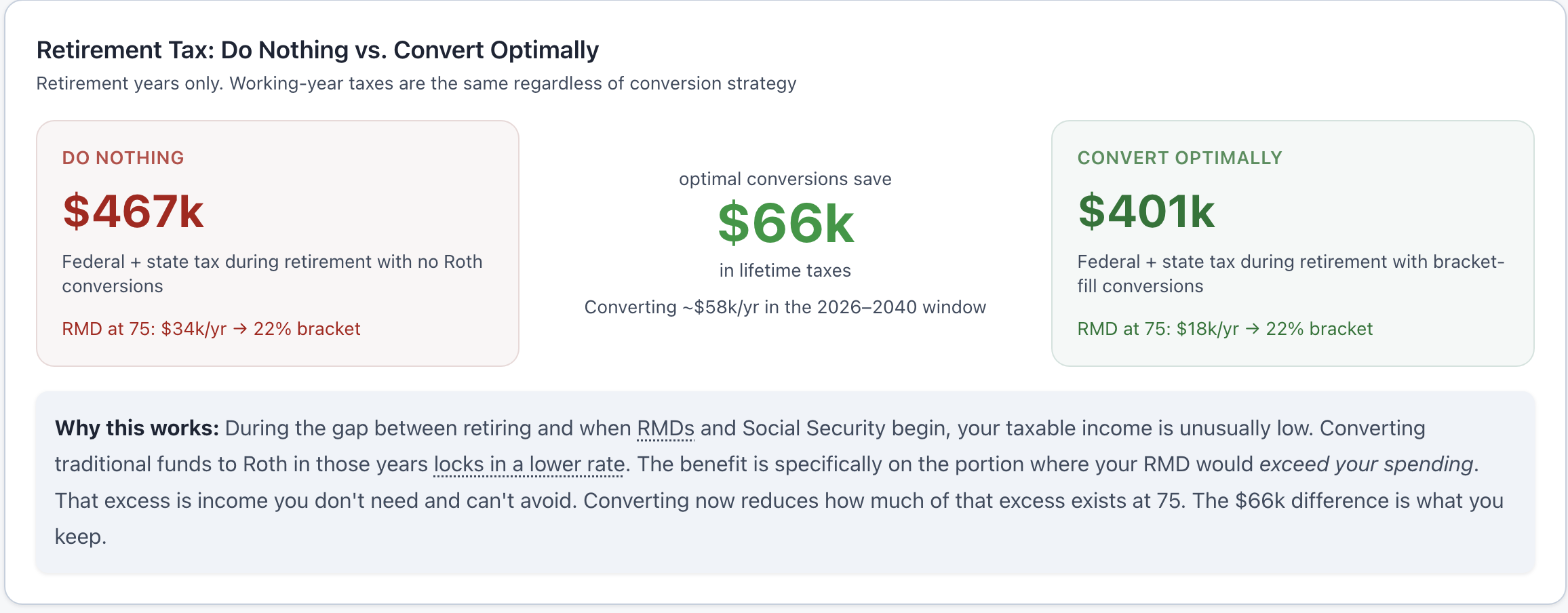

Roth 401(k) accounts are exempt from required minimum distributions under SECURE Act 2.0, which eliminated the Roth 401(k) RMD requirement starting in 2024. This means you are never forced to withdraw from a Roth account during your lifetime, which is a significant advantage for tax planning in your 70s and beyond.

The marginal vs effective rate question

Your marginal rate is the rate on your last dollar earned. Roth contributions save you tax at the marginal rate now (the top bracket you are in), while pretax withdrawals in retirement are taxed at your effective rate, which is the average across all brackets. The first dollars you withdraw in retirement fill the 0% bucket (the standard deduction), then 10%, then 12%, and so on. So even if your marginal rate in retirement equals your marginal rate today, pretax can still win because some of those retirement dollars are taxed at very low rates.

This cuts both ways. If you already have substantial pretax savings, the low-bracket advantage diminishes because RMDs and Social Security may already be filling those brackets for you. Additional pretax contributions in that case may end up taxed at your highest rate anyway.

After-tax outcome by retirement bracket

The table below shows the after-tax value of a $20,000 pretax contribution growing at 7% annually for 25 years, then taxed at different retirement brackets. For comparison, it shows the equivalent Roth contribution made by someone currently in the 22% bracket. It uses the same gross dollars after paying today's tax first.

| Contribution | Balance at withdrawal | Rate at withdrawal | After-tax value |

|---|---|---|---|

| Pretax $20,000 | $108,548 | 12% in retirement | $95,522 |

| Pretax $20,000 | $108,548 | 22% in retirement | $84,667 |

| Pretax $20,000 | $108,548 | 32% in retirement | $73,813 |

| Roth $15,600 (22% paid today) | $84,667 | Tax-free | $84,667 |

Pretax balance = $20,000 × (1.07)^25 = $108,548. Roth balance = $15,600 × (1.07)^25 = $84,667, where $15,600 is $20,000 after 22% tax paid today. If you expect to be in the 12% bracket in retirement, pretax wins by over $10,000. If you expect the 32% bracket, Roth wins by the same margin. Both are exactly equal when today's rate matches the retirement rate.

When pretax usually wins

Pretax contributions make the most sense during peak earning years when you are in the 32% bracket or higher. If your income will fall significantly in retirement because you are reducing expenses, living on Social Security and modest withdrawals, or moving to a state with no income tax, the gap between what you pay now and what you pay later can be substantial. For someone dropping from a 32% marginal rate today to a 12% effective rate in retirement, pretax contributions save roughly $4,000 in tax for every $20,000 contributed compared to Roth.

Pretax also works well when you have limited savings so far and expect to draw only modest amounts in retirement. Low withdrawals mean low marginal rates, and the low-bracket fill advantage of pretax is strongest when your retirement income is not already crowded by Social Security and forced RMDs.

When Roth usually wins

Roth contributions are strongest when your current marginal rate is low, which is most common early in your career, in years with income dips, or when one spouse is not working. If you are in the 12% bracket today, you may never see rates that favorable again. Locking in that rate through Roth contributions is usually the right choice.

Roth also wins when you already have substantial pretax savings. A large traditional 401(k) balance heading into retirement means large RMDs starting at age 72, 73, or 75 (depending on your birth year). When Social Security is added on top, your effective tax rate in retirement may be higher than you expect, even if your spending is modest. Every additional pretax contribution to a balance that will already generate high RMDs is a dollar taxed at your worst rate. More Roth in that situation gives you tax-free income to draw alongside the forced traditional withdrawals.

Future tax rate uncertainty also favors Roth. The tax cuts from the 2017 Tax Cuts and Jobs Act are scheduled to expire after 2025, which would push today's brackets upward. Roth locks in your tax liability now and removes the risk that rates rise before you retire. And for anyone planning to leave money to heirs, Roth is particularly valuable: a Roth account inherited by a child in their 40s or 50s continues growing tax-free, while a traditional IRA must be emptied within 10 years of your death and taxed at the heir's ordinary income rate during what are often their highest-earning years.

The split strategy

Many planners recommend splitting contributions between pretax and Roth as a hedge against future tax uncertainty. Having both account types gives you flexibility in retirement: you can withdraw from pretax in low-income years and from Roth in high-income years to manage which bracket you land in each year. A common approach is to contribute pretax up to the employer match, then go Roth for the rest. If you are in the 12% bracket, there is a strong case for going all Roth. You may never be in a lower bracket again.

ThunderHarbor's 401(k) Optimizer tab models both pretax and Roth contribution scenarios with your actual balances and income, projecting the year-by-year after-tax outcome across your full retirement. It accounts for your state's tax treatment, expected Social Security income, and RMD projections, so the comparison reflects what you will actually keep rather than a simplified rate-on-rate estimate.

Not financial advice

This guide is for informational purposes only. Nothing here constitutes financial, tax, or legal advice. Always consult a qualified professional before making significant financial decisions.

See the actual numbers for your situation

ThunderHarbor's 401(k) Optimizer models pretax vs Roth contributions with your actual balances, income, state taxes, and RMD projections, showing the lifetime after-tax difference.

Build your free planFree plan included · Full 401(k) optimizer with Premium ($47/year)