Inherited IRA Rules and Strategies: The 10-Year Rule Explained

Leaving a traditional IRA to your kids used to mean they could stretch withdrawals across their own lifetime, paying tax gradually over decades. The SECURE Act changed that for most beneficiaries. Today, a large traditional balance can turn into a forced, decade-long tax event for the people you leave it to, often during their highest-earning years. Here is what the rules actually say, and what you can do about it now.

The 10-year rule

Under the SECURE Act, most non-spouse beneficiaries who inherit a traditional IRA, 401(k), or similar account must withdraw the entire balance by December 31 of the tenth year after the original owner's death. There is no requirement to spread withdrawals evenly, you could technically wait until year 10 and take it all at once, but doing so usually creates the worst possible tax outcome by stacking a decade of income into a single year.

If the original owner had already begun taking required minimum distributions before they passed away, the IRS generally requires the beneficiary to continue taking annual RMDs throughout the 10-year window, on top of fully emptying the account by the deadline. This detail catches many beneficiaries off guard, and missing an RMD carries the same percentage penalty that applies to original owners.

Who is exempt: eligible designated beneficiaries

Not everyone is subject to the 10-year rule. The IRS carves out a category called "eligible designated beneficiaries" who can generally still stretch withdrawals across their own life expectancy, much like the old rules allowed. This group includes surviving spouses, minor children of the account owner (until they reach the age of majority, at which point the 10-year clock starts), beneficiaries who are disabled or chronically ill, and beneficiaries who are not more than 10 years younger than the original owner.

Surviving spouses also have a unique option: they can treat an inherited IRA as their own, rolling it into their own account and following the normal rules that would apply to any IRA they owned themselves, including being able to wait until their own RMD age to begin withdrawals.

Why the tax bill can be so much larger than expected

Every withdrawal from an inherited traditional IRA is taxed as ordinary income to the beneficiary, in the year they take it. Compressing an entire balance into a 10-year window, often while the beneficiary is in their 40s, 50s, or early 60s and at their peak earnings, can push a moderate inheritance into the highest brackets the beneficiary will ever see.

A $500,000 traditional IRA inherited by an adult child in their peak earning years can easily generate well over $150,000 in additional federal and state tax across the 10-year period, money that a combination of lifetime Roth conversions and careful withdrawal timing could have substantially reduced.

Strategies for the original account owner

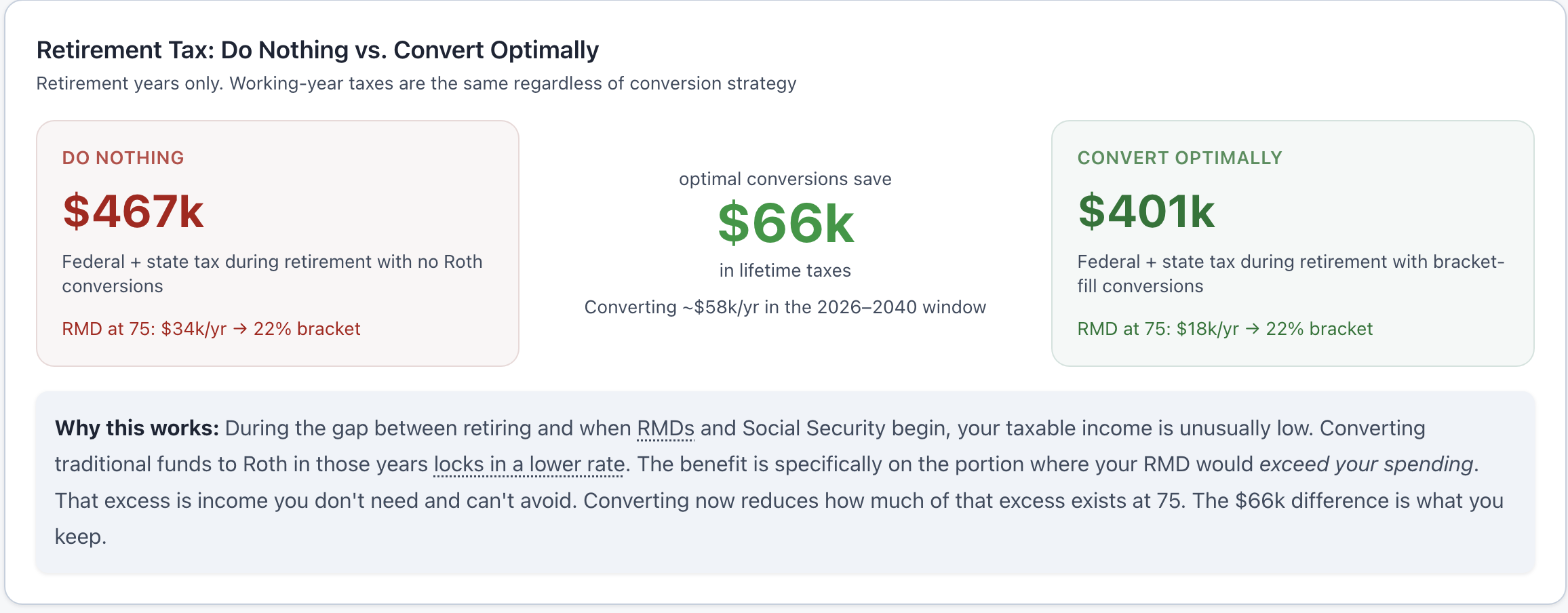

The single most effective lever is often Roth conversion during your own lifetime. Inherited Roth IRAs are still subject to the 10-year emptying rule for most beneficiaries, but the withdrawals are tax-free, since you already paid the tax at conversion. Converting a traditional balance to Roth during your low-income retirement years can shift a large future tax bill from your heirs' peak-earning years to your own lower-bracket years.

Qualified charitable distributions are another option if you are charitably inclined, since they reduce your traditional balance (and your own RMDs) without generating taxable income for you or shrinking what eventually passes to non-charitable heirs from other assets. For households with both traditional and Roth balances, deciding who inherits which account, and how to title beneficiaries, can also meaningfully change the outcome.

Strategies for the beneficiary

If you are the one inheriting the account, the goal is to spread withdrawals across the 10-year window in a way that avoids spiking into a higher bracket in any single year. That often means taking distributions earlier, in years when your other income is lower, rather than waiting until the deadline forces a large lump-sum withdrawal. It can also mean coordinating the timing with your own retirement, RMDs, and Social Security claiming decisions, since all of these interact on the same tax return.

Not financial advice

This guide is for informational purposes only. Nothing here constitutes financial, tax, or legal advice. Inherited IRA rules are complex and depend on your specific situation. Always consult a qualified professional before making significant financial decisions.

See what your heirs would actually owe

ThunderHarbor's Inherited IRA Analyzer projects the 10-year withdrawal schedule and estimated tax cost, so you can see how much lifetime Roth conversions could save your heirs.

Build your free planFree plan included · Inherited IRA Analyzer with Premium ($47/year)