The DIY Retirement Planning Guide

The core retirement decisions are fundamentally mathematical: how much to save, when to retire, and how to minimize taxes. Tax brackets are published by the IRS. RMD amounts follow a fixed table. Social Security benefits follow a formula based on your 35 highest-earning years. These are calculations, and a computer can run them faster and more accurately than any human working from a spreadsheet or a binder of projections.

Why plan your own retirement

A comprehensive financial plan from a certified financial planner costs $2,000–$5,000 upfront, plus ongoing advisory fees of 0.5–1% of assets under management. For someone with $500,000 saved, that is $2,500–$5,000 per year, every year, for advice that often amounts to generic asset allocation and a set of projections printed once and never updated.

DIY planning does not mean guessing. It means using tools that model your specific situation: your balances, your income, your state's tax rules, and your expected retirement age. These tools show the year-by-year outcome of each decision before you make it. The math has always been accessible. What changed is that software can now run it connected across all the variables at once, rather than treating each decision in isolation.

The five decisions that matter most

Most retirement advice overwhelms you with dozens of variables. In practice, five decisions drive the vast majority of your outcome.

How much you save

Your savings rate is the single biggest lever. Most people need to save 15–20% of gross income to maintain their lifestyle in retirement. If you are behind, this is the first number to change.

Pretax vs Roth contributions

This determines when you pay tax, now or later. If your current marginal rate is low (early career, or one spouse not working), Roth is often the better bet. If you are in your peak earning years, pretax saves more immediately.

When you retire

Retiring at 62 vs 67 vs 70 changes everything: Social Security amounts, years of withdrawals, healthcare coverage, and how long your money needs to last. Even one extra year of work can add $100k or more to your portfolio and increase Social Security by 8%.

When you claim Social Security

Delaying from 62 to 70 increases your monthly benefit by about 77%. For married couples, the coordination between spousal and survivor benefits can mean tens of thousands of extra dollars per year for the surviving spouse.

Roth conversion strategy

The years between retirement and your RMD start age (72, 73, or 75 depending on your birth year), when RMDs begin, are your conversion window. Converting the right amount each year, enough to fill your bracket without triggering IRMAA, can save hundreds of thousands in lifetime taxes.

What you need to model

A real DIY plan is not just savings times a growth rate equals a future number. You need to model the interactions between multiple systems that most people, and even most advisors, treat separately.

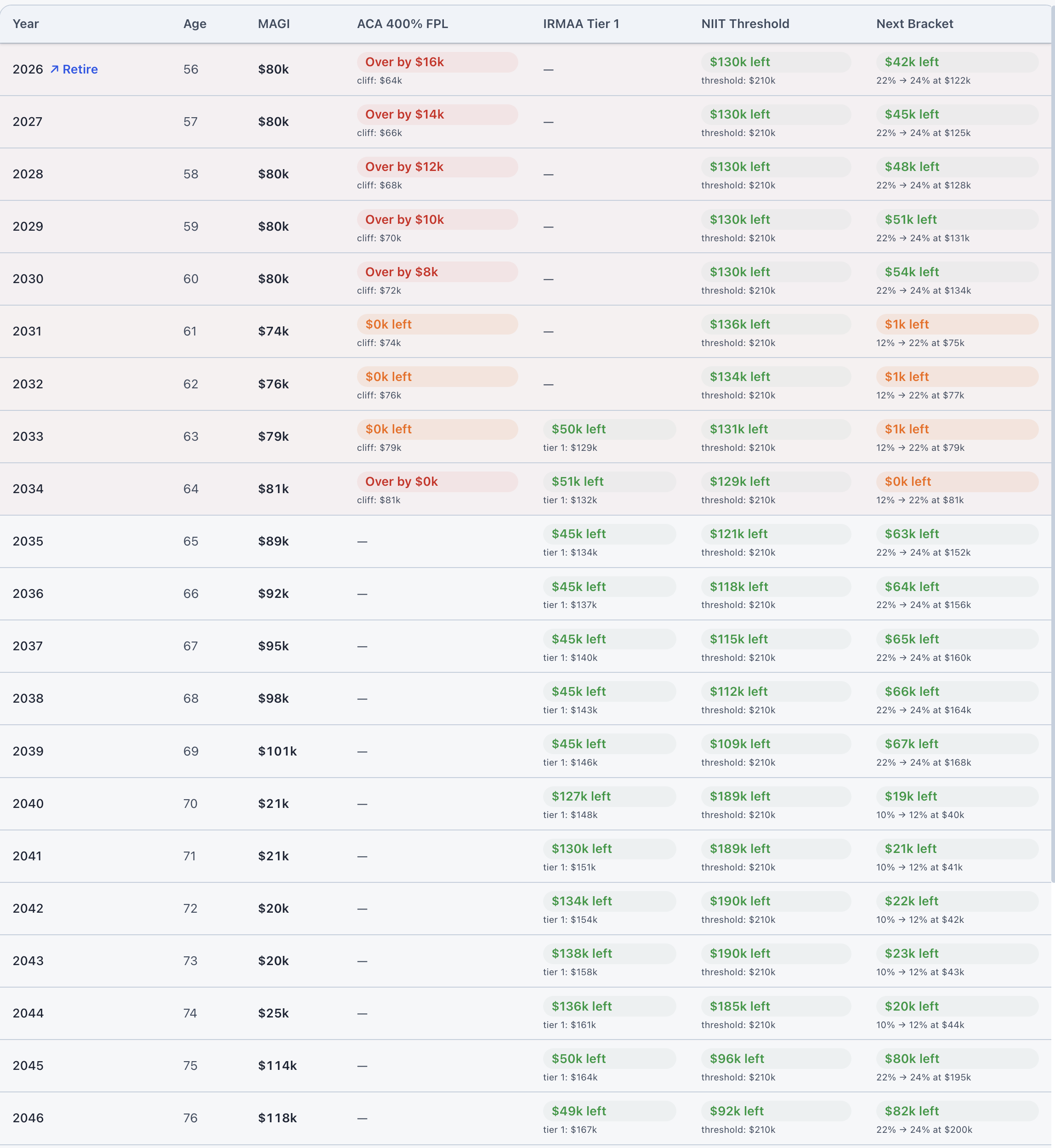

Federal taxes are the first system. Each year's withdrawals, Social Security income, and any earned income push you into different brackets. The order you withdraw from accounts changes which bracket you land in and how much of your benefit gets taxed. A $70,000 withdrawal from a traditional IRA in a year when Social Security is also flowing can put you in a 22% bracket on income you would have taxed at 12% had you drawn from Roth instead.

RMDs are the second system. Starting at age 72, 73, or 75 (depending on your birth year, under SECURE Act 2.0), the IRS forces you to withdraw a percentage of your traditional account balance each year regardless of whether you need the money. At 73 that percentage is roughly 3.8% and it rises every year. A couple with $1.5 million in traditional accounts will face combined RMDs of over $56,000 per year at RMD start, stacked on top of Social Security, whether they planned for it or not.

Medicare IRMAA is the third. Income above certain thresholds triggers surcharges on Medicare Part B and D premiums, up to $600 or more per person per month above the standard cost. Because the surcharge is based on your income from two years prior, a large Roth conversion or traditional withdrawal today shows up in your Medicare bill two years from now. Your conversion strategy needs to model this lookback explicitly.

ACA marketplace subsidies are the fourth if you retire before Medicare begins at 65. Premium tax credits are calculated as a percentage of the Federal Poverty Level, and crossing 400% FPL eliminates the entire subsidy with a single dollar of extra income. A Roth conversion that crosses that line in a year when you are on marketplace insurance can cost more in lost subsidies than the tax benefit of converting.

Social Security taxation is the fifth. Up to 85% of your Social Security benefit can be subject to federal income tax depending on your combined income. The thresholds are not indexed for inflation, which means more retirees cross them each year. The timing of your other withdrawals directly affects how much of your benefit you keep. No single one of these systems is complicated on its own. The challenge is modeling how they interact across 30 years, and that is precisely what ThunderHarbor does.

How ThunderHarbor maps to each decision

ThunderHarbor is built around the specific planning decisions that move the needle most. Every major tab connects to a concrete retirement question. The table below maps the key decisions from this guide to the tool that handles them.

| Planning decision | ThunderHarbor tool |

|---|---|

| Pretax vs Roth contribution split | 401(k) Optimizer |

| When to claim Social Security | Social Security tab |

| Roth conversion timing and amount | Roth Strategy tab |

| RMD projections and tax impact | RMD Analyzer |

| IRMAA and ACA cliff exposure | Tax Cliffs tab |

| Early retirement bridge income (before 59½) | SEPP Planner |

| Inherited IRA tax cost for heirs | Inherited IRA Analyzer |

| Market volatility and portfolio durability | Monte Carlo Risk |

| Healthcare costs and spending by life phase | Life & Spending tab |

| Large one-time purchases and their impact | What-If Workshop |

| Comparing two retirement paths side by side | Compare Scenarios |

| Estate and legacy planning | Legacy Planning tab |

All tools share the same underlying projection, so a change in one place, whether it is your Social Security claiming age, a Roth conversion amount, or a spending adjustment, flows through every other tab automatically.

When to get professional help

DIY planning works well for most straightforward situations: W-2 income, 401(k) and IRA savings, standard Social Security timing. If your situation involves complex estate planning, business ownership, stock options, pension elections, or multi-generational wealth transfers, a good advisor earns their fee on those specific questions.

The most efficient approach for many people is a hybrid: use tools to understand the math and form your own views, then validate your plan with a fee-only advisor, one you pay by the hour, not one who takes a percentage of your assets. You will get better advice because you are starting from an informed position, and you will spend less because you have already done the heavy lifting. ThunderHarbor's year-by-year projection and concern-aware summary report give you a clear document to bring into that conversation.

Not financial advice

This guide is for informational purposes only. Nothing here constitutes financial, tax, or legal advice. Always consult a qualified professional before making significant financial decisions.

Run the full year-by-year projection with your numbers

ThunderHarbor models all five decisions together: taxes, Social Security, RMDs, IRMAA, Roth conversions, and portfolio longevity, all connected in one projection with your actual data.

Build your free planFree plan included · Full planning suite with Premium ($47/year)