May 29, 2026

Your Retirement Projection Is Only as Good as Your Spending Number

The single most important input in any retirement projection is not your account balance or your expected rate of return. It is your annual spending. Everything else flows downstream from that one number. How long the money lasts, how large the required minimum distribution becomes, how much of Social Security is taxable, whether IRMAA Medicare surcharges apply. Most retirement tools let you enter it once, during onboarding, and leave it there forever. That number is always a guess. When the guess drifts from reality, the entire projection quietly runs on a flawed foundation. And nobody tells you.

Why spending is the load-bearing assumption

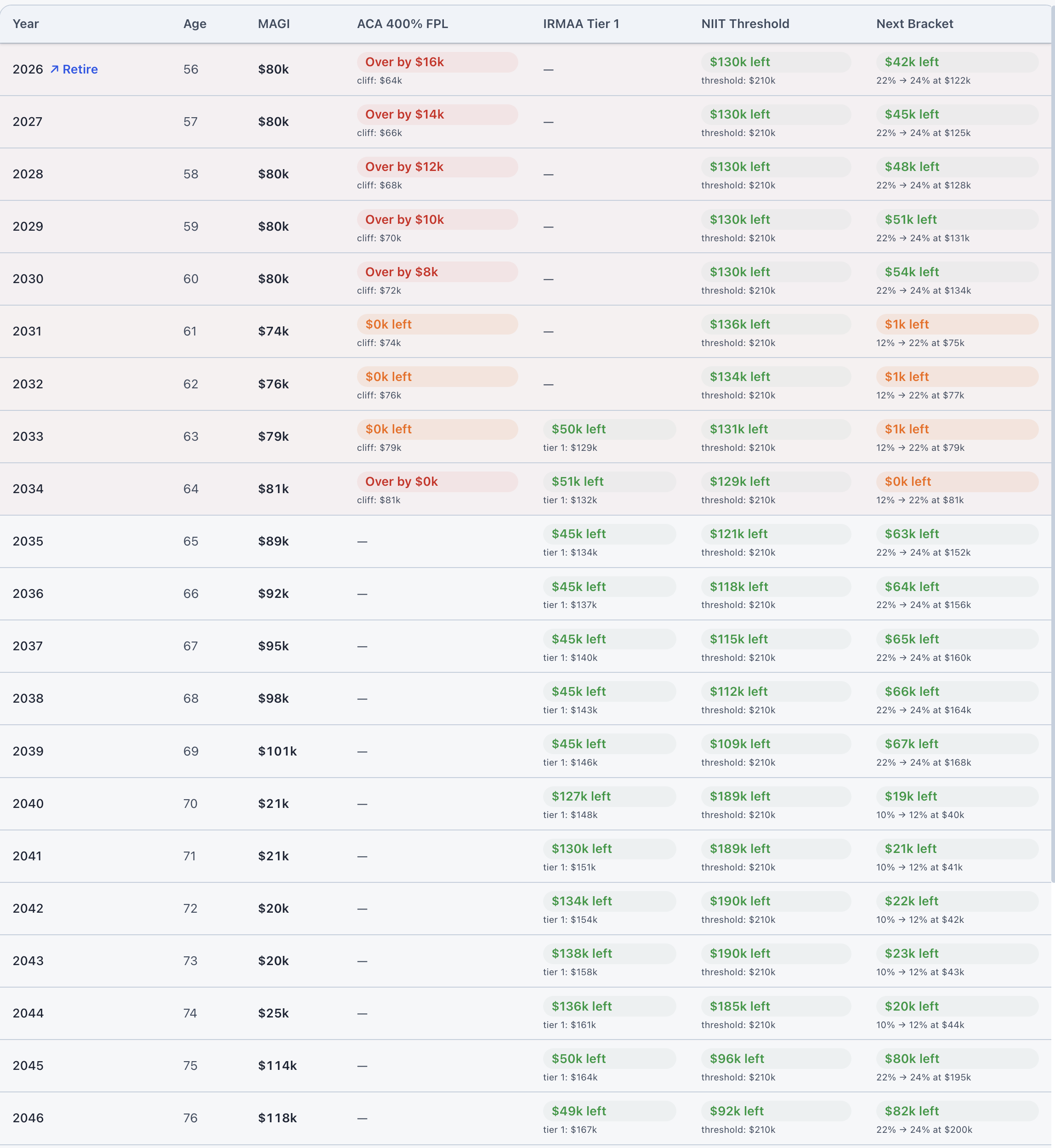

When a retirement engine runs a 25-year projection, it uses your spending target to determine how much the portfolio needs to generate each year. If your Social Security and pension cover part of it, the engine draws the rest from your accounts in a sequence that affects your taxable income, your MAGI, your Roth conversion headroom, and ultimately your Medicare premiums two years later. Every one of those decisions chains back to the spending number.

A spending estimate that is $20,000 per year too high does not just make your portfolio depletion date look earlier than it really is. It also makes every projected IRA withdrawal look larger than it will be, which overstates your projected MAGI, which overstates the likelihood of IRMAA surcharges, which may push the Roth conversion recommendation higher than your situation actually requires. The error compounds across 25 years and affects every output the projection produces.

The reverse is equally true and equally important. A spending estimate that is $20,000 per year too low understates how hard the portfolio is working. The projection looks more comfortable than it is. Roth conversion headroom appears to exist when it has actually been consumed by real spending. The person who trusts that projection may convert less than they should, or feel more secure than the numbers warrant.

Case study: Patricia, who was spending more than she thought

Patricia is 67 and retired two years ago. When she set up her retirement plan, she estimated $6,000 per month in spending, or $72,000 per year. That felt right. Her mortgage was paid off, the kids were gone, and she had always been careful with money. She entered the number, the projection looked solid, and she moved on.

Her first full year of retirement came in at $93,600. A bathroom remodel she had been putting off, two trips she had been promising herself for a decade, and a car repair that could not wait. None of it was reckless. All of it was real. The gap between plan and reality was $21,600 in year one alone.

To cover the difference, Patricia drew more from her traditional IRA than the projection expected. That additional withdrawal was fully taxable income. Her MAGI for the year landed $18,000 higher than projected, enough to push her into the next IRMAA tier. Medicare applied the surcharge to her Part B and Part D premiums two years later. The extra cost was $816 for the year. Not devastating, but not something she planned for or saw coming either.

More importantly, her projection was still showing $72,000 per year. Her projected IRA balance at 73, her estimated RMD, her expected tax bracket in her early seventies. All of it was built on a spending assumption her real life had already disproved. She had no way to know her plan needed to be recalibrated until she logged what actually happened.

Case study: Robert, who discovered conversion headroom he did not know he had

Robert is 65 and retired at the beginning of the year. His plan called for $8,000 per month, which is $96,000 per year and roughly what he had been spending in the last few years of his working life. His projection showed comfortable but not lavish runway, and he had been planning to convert roughly $30,000 per year from traditional to Roth to manage his eventual RMD.

Six months into retirement, his actual monthly spending was running closer to $6,200. The commuting costs were gone. He was cooking at home more. Two recurring expenses he had forgotten about had both quietly lapsed: a gym membership and a professional subscription he no longer needed. His real spending was $74,400 annualized, not $96,000. The difference was $21,600 per year.

That gap changed his plan in a meaningful way. His IRA draws were smaller than projected, which meant his MAGI was lower than his plan assumed. He was well below the next IRMAA tier. He had $21,600 per year in additional Roth conversion headroom that his original projection did not show, because his original projection did not know his real spending. Converting that headroom each year, at current rates in a low-income period before Social Security starts, was exactly the kind of opportunity his plan was designed to find. His plan just did not know it existed.

Both Patricia and Robert had the same underlying problem. Their plans were running on a number that had stopped being accurate the moment they started living differently from how they expected. Neither plan was broken. Both plans were simply working from outdated information.

Which account you draw from is just as important as how much

There is a second dimension that most spending trackers ignore entirely: the source of the money. The same $93,600 in annual spending can have a dramatically different effect on your retirement projection depending on which accounts covered it.

If Patricia drew her $93,600 entirely from her traditional IRA, the full amount counts as ordinary taxable income. It flows directly into MAGI. It affects her ACA subsidy if she is under 65, her IRMAA tier, and how much of her Social Security income is taxable once SS begins. If she drew the same $93,600 from a Roth IRA instead, none of it hits her MAGI. Zero impact on IRMAA. Zero impact on SS taxability. Same spending, same lifestyle, completely different tax picture.

A taxable brokerage account sits in between. Long-term capital gains are partially taxable and do flow into MAGI, but at lower rates than ordinary income and often at 0 percent for people in the 12 percent bracket. The account you draw from is not a minor detail. For someone managing IRMAA exposure or an ACA subsidy cliff, it can be the entire decision.

This is why tracking the total spent in a month is necessary but not sufficient. The projection needs to know where the money came from to correctly calculate taxable income, MAGI, and every downstream number that depends on them.

How ThunderHarbor's On Track feature works

We are not trying to build a budget tracker. Nobody wants to log every grocery receipt. What we built is something narrower and more useful for retirement specifically: once a month, you record your total spending and which accounts you actually drew from. That is it. Two to three fields, two minutes, once a month.

Those numbers feed directly into the projection engine. The spending estimate you entered during onboarding becomes the baseline, your starting point. The monthly actuals become the reality. The engine compares them, annualizes the actuals based on how many months you have recorded, and runs the full projection forward from real data instead of a standing assumption. Every downstream number updates automatically. RMD projections, tax estimates, Medicare costs. All of it reflects what is actually happening, not what was expected at the start.

For Patricia, logging her actual $7,800 per month immediately recalibrated the projection. The engine recalculated her IRA draws based on real spending, updated her projected MAGI, flagged the IRMAA exposure, and showed the revised portfolio trajectory. All in the same place she had always been looking at her plan. For Robert, logging $6,200 per month surfaced the conversion headroom. The app showed him his actual MAGI for the current year, the gap to the next IRMAA tier, and the additional conversion he could execute before year end. A number he had been leaving on the table became visible.

The feature only appears once you are retired. It is not designed for the accumulation phase. During accumulation, the spending number matters less because the portfolio is still growing and the income picture is dominated by salary. In retirement, when every dollar of spending comes directly from the portfolio or from taxable income, the accuracy of that number determines the accuracy of everything else.

The compounding value of a real number

A retirement projection that runs for 25 years has a lot of room to drift. An error in year one compounds through every subsequent year. The projection that told you your money lasts to 95 was computed from inputs that may have been reasonably accurate the day you entered them and gradually less accurate every year after that.

Logging one real number per month does not solve every uncertainty in retirement planning. Returns are still unknown. Tax law can change. Health costs are unpredictable. But spending is the one input you actually know. You lived it. You have the bank statement. It is the one place where a retirement plan can stop guessing and start reflecting reality. That is worth more than any improvement to the assumed return rate.

The onboarding estimate is still useful. It gives the plan a starting point and a reference to compare against. But the moment you start logging real months, the projection stops running on hope and starts running on evidence. The further the actuals diverge from the estimate, in either direction, the more valuable that recalibration becomes.

Not financial advice

This article is for informational purposes only. Case study characters and numbers are illustrative and use simplified assumptions. Your actual projected spending, MAGI, IRMAA exposure, and portfolio trajectory depend on many factors including market returns, tax law changes, and personal circumstances. Always consult a qualified financial professional before making significant decisions.

See how your actual spending changes the projection

ThunderHarbor's On Track feature lets you log real monthly spending and which accounts you drew from. The projection updates automatically. Your RMD estimates, tax picture, and Medicare costs reflect what is actually happening, not what you guessed at the start.

Run your projection