May 17, 2026

When to Switch to a Roth 401k: What the Rules of Thumb Actually Miss

At some point, most people who are serious about retirement planning ask the same question. Should I be putting my 401k contributions into the traditional bucket or the Roth bucket? The internet gives a fast answer: if you are in a high tax bracket now, go traditional. If you expect to be in a higher bracket later, go Roth. That answer is not wrong exactly, but it is so incomplete that following it blindly can cost you more than you realize. There are several factors that rarely come up in the casual version of this conversation, and for high earners in particular, those overlooked factors often change the conclusion entirely.

The baseline logic and why it does not always hold

The standard argument for traditional 401k contributions goes like this. You are earning well now, so your marginal tax rate is high. Deferring income into a traditional account saves you taxes at that high rate today. When you retire, your income drops, your bracket drops, and you withdraw at the lower rate. You pocket the difference.

For a significant portion of the population, that story is accurate. If you earn modestly now and expect to live on modest withdrawals in retirement, traditional contributions genuinely move money from a higher tax environment to a lower one. The math works in your favor, and the conventional advice is correct.

The problem is that the story quietly falls apart for a different group of people, and that group is larger than most financial content acknowledges. If you are a higher earner who has been consistently maxing out your 401k for the past decade or two, your traditional balance is already large enough that the math has shifted. Your retirement bracket is not determined only by the income you choose to take out. It is increasingly determined by income you are forced to take out, whether you need it or not.

The 3x rule and what it is actually trying to tell you

You may have heard a rule of thumb that circulates in personal finance circles: if your traditional 401k balance has reached roughly three times your annual salary by the time you are 40, you should start shifting your new contributions toward Roth. The idea behind it is reasonable even if the specific number is rough. At three times your salary, compounding alone over the next 25 to 30 years will push your traditional balance to a level where the required distributions in your seventies could exceed your inflation-adjusted spending, creating forced taxable income above what you actually need.

Take a concrete example. Someone earning $200,000 who has $600,000 in a traditional 401k at 40 and keeps contributing at roughly current maximums will realistically have somewhere between $4 million and $6 million in that account by age 73 or 75, depending on market returns. The IRS requires withdrawals starting at 73 or 75 (depending on birth year) based on a life expectancy table. On a $5 million traditional balance, the first year’s required distribution is roughly $189,000. That income lands on your tax return regardless of your other choices, and it lands on top of Social Security, any pension, and whatever else you have.

The 3x rule is a proxy for a more specific question: will your RMD at RMD start age exceed your inflation-adjusted spending? If it does, that excess is forced income you did not choose to take, and it is taxed unnecessarily. Once your traditional balance is large enough that compounding alone will generate RMDs meaningfully above your retirement spending, you have moved from “defer now, pay less later” into “defer now, pay on income you did not even need.” That is the precise situation where Roth conversions add value.

But the 3x threshold is not a universal law. Someone earning $80,000 with $240,000 in traditional accounts is in a very different position than someone earning $300,000 with $900,000. The rule uses salary as a rough proxy for your retirement spending level and your likely Social Security income, but those assumptions break down at the extremes. For very high earners, the threshold that triggers a real RMD problem is often lower in salary multiples than 3x, because their balances grow faster and their Social Security and other income sources are already high on their own.

Why high earners face a different version of this question

For someone in the 32 or 37 percent federal bracket today, the classic argument for traditional contributions is strongest on the surface. You are clearly paying a high rate now, and surely retirement will be cheaper. The trouble is that “surely” is doing a lot of work in that sentence, and it often is not earned.

High earners tend to have high Social Security benefits from decades of above-average wages. They tend to have sizable taxable brokerage accounts that generate dividends and capital gains every year even in retirement. They often have pensions or other income streams. And if they have been contributing heavily to a traditional 401k, they have the RMD problem described above. Stack all of those income sources together in retirement and the marginal bracket is not necessarily lower than it was during peak earning years. For some households it is higher.

When we model this in ThunderHarbor for high-income users with large traditional balances and substantial retirement spending needs, we frequently see a pattern where the deferral saves 24 percent today and the same dollars come out at 24 to 32 percent later, because their inflation-adjusted spending requires large withdrawals anyway, and the RMD exceeds that spending, stacking excess income on top. The deferral did not move them to a lower bracket. It delayed the same bracket while removing flexibility about the timing.

That changes the math significantly. If you are saving 24 cents per dollar today by contributing to traditional, but you are going to pay 24 to 32 cents per dollar when it comes back out, the Roth contribution starts to look considerably more attractive even though you are in a high bracket right now.

The piece that almost nobody talks about: what happens when you die

There is a factor in this decision that gets almost no attention in popular retirement content, and it can shift the answer significantly for anyone who intends to leave money to children or other non-spouse heirs.

Before 2020, inherited IRAs had a stretch provision that allowed heirs to take distributions over their own lifetimes, spreading the tax hit across decades. The SECURE Act eliminated that. Today, when a non-spouse heir inherits a traditional IRA or 401k, they must withdraw the entire balance within ten years. There are no minimums per year, but the account must be empty by year ten. For most working-age heirs, that means pulling out large taxable distributions during years when they are earning their own salaries, which means those inherited dollars often get taxed at the heir’s highest marginal rate.

A child in their forties earning $150,000 who inherits a $1.5 million traditional IRA has to pull out roughly $150,000 per year for a decade on top of their existing income. That pushes them from the 22 or 24 percent bracket into the 32 or 35 percent bracket for ten years. The inheritance, which might have been intended as a meaningful gift, ends up with the IRS taking a third or more of it.

A Roth account passed to the same heir follows the same ten-year rule but with one critical difference: the distributions are completely tax-free. The heir still has to pull the money out within ten years, but none of it adds to their taxable income. For a parent who cares about what actually reaches their children versus what goes to taxes, this distinction can be worth more than all the bracket optimization that happened during the accumulation years.

This is why ThunderHarbor’s planning engine weighs the legacy picture alongside the tax picture. When someone has a large traditional balance, a high-earning adult child, and a desire to leave a meaningful inheritance, the answer often tilts toward Roth even when the simple bracket comparison might suggest traditional. The account type affects not just your taxes in retirement but the effective tax cost to your family over the following decade.

IRMAA: the bracket-within-a-bracket that catches people off guard

There is one more factor worth naming, because it consistently surprises people who have planned carefully for income taxes but not for Medicare. Once you are on Medicare, your premiums for Part B and Part D are tied to your income from two years prior. The income thresholds that trigger higher premiums are called IRMAA, and they step up in tiers. Above certain income levels, a couple can pay thousands of dollars more per person per year compared to someone with slightly lower income.

RMDs are counted as ordinary income for IRMAA purposes. So a household that has a modest investment income and Social Security income might be sitting just below an IRMAA threshold for most of their retirement, only to have their first RMD push them over it. A large traditional balance does not just create an income tax problem. It creates an IRMAA problem that can add four to eight thousand dollars per couple per year in higher Medicare premiums, year after year.

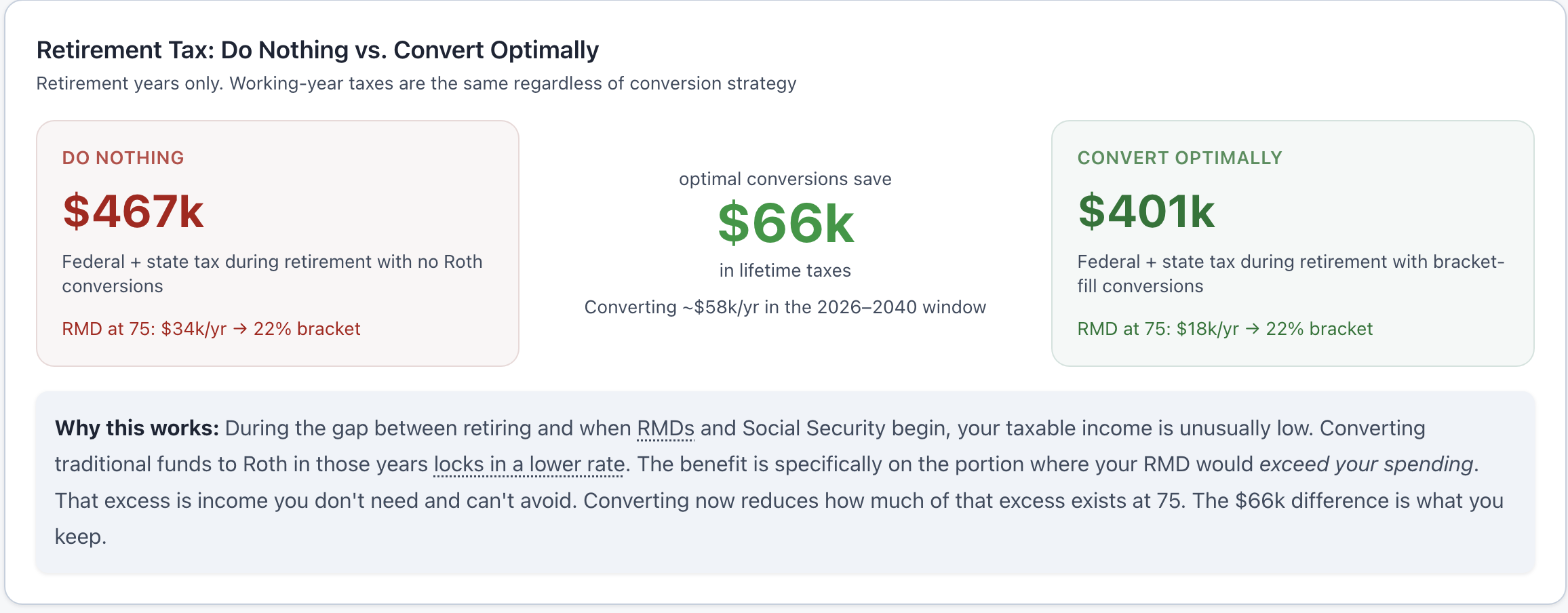

Roth withdrawals do not count toward IRMAA calculations. They do not count toward the provisional income formula that determines how much of your Social Security gets taxed either. For someone who is right around an IRMAA threshold or near the point where additional income would make more of their Social Security taxable, shifting future contributions to Roth and doing Roth conversions in the gap between retirement and 73 can preserve a level of Medicare premium efficiency that traditional contributions make impossible.

What you actually need to know to make this decision well

The honest version of this question requires knowing several things that are not that hard to pull together but that most people have not done. What is your current marginal federal and state tax rate, calculated correctly after your actual deductions, not just based on what bracket your gross income appears to be in? What will your traditional balance be at retirement, assuming you keep contributing at your current rate and earning roughly historical returns? What will the required distribution on that balance be when you are 73, and what does that add to your other expected income? And separately, do you intend to pass money to heirs who are in their own working years?

Each of those inputs changes the conclusion. Someone who is in the 22 percent bracket with a modest traditional balance and no particular legacy intention is probably fine with continued traditional contributions. Someone in the 22 percent bracket who already has a large traditional balance and earns enough that their RMDs will push them back to 24 or 32 percent is in a genuinely different situation, even though the current bracket looks the same on the surface.

The 3x rule is a useful prompt to ask the question, not a reliable answer to it. It tells you when the math is likely to have shifted enough that Roth deserves a serious look. It does not tell you how much to shift, or whether your specific combination of income, balance, state tax, Social Security, and legacy wishes actually favors Roth. For that, you need the full projection.

The other thing worth saying plainly is that this is not a one-time decision. The right answer at 38 may not be the right answer at 45, and almost certainly is not the right answer at 52. Your income changes. Your balance grows. Your retirement date gets closer and the projection becomes more precise. Revisiting the contribution type every few years, or when something significant changes in your financial picture, catches most of the error that comes from setting a default and forgetting about it.

If there is a single sentence that holds most of the time for the ThunderHarbor audience of higher earners with sizable existing balances, it is this: you are probably not going to be in as low a bracket in retirement as you think, your heirs are probably going to pay a higher rate than you expect on what they inherit, and both of those facts push the answer further toward Roth than the simple conventional wisdom suggests. But the only way to know for your specific situation is to actually run the numbers.

Not financial advice

This article is for informational purposes only. Nothing here constitutes financial, tax, or legal advice. Tax brackets, Medicare thresholds, and contribution limits change year to year. The SECURE Act rules described here are current as of 2026. Always consult a qualified professional before making significant financial decisions.

See how this plays out with your actual numbers

ThunderHarbor projects your traditional balance to RMD age, estimates your forced income at 73, models the IRMAA impact, and shows the legacy tax cost to your heirs, so the contribution decision is based on your full picture, not a rule of thumb.

Start your free plan