June 2, 2026

Roth Conversion Ladder vs 3-Bucket Method: The Hidden ACA Cost Nobody Calculates

The Roth conversion ladder gets a lot of attention in FIRE communities. The idea sounds clean: convert chunks of your traditional IRA to Roth each year, pay the tax now, wait five years, and pull that money out penalty-free before you turn 59 and a half. It solves one real problem. But for most early retirees it quietly creates a much bigger one, and that bigger problem does not show up in any calculator that only looks at taxes and penalties. It shows up in your health insurance bill.

Health Insurance Is the Largest Expense Most Early Retirees Underplan For

If you retire before 65, you are on your own for health insurance until Medicare begins. An unsubsidized ACA plan for someone in their fifties can run $900 to $1,400 per month per person. For a couple, that is easily $20,000 to $30,000 per year at full price.

The ACA premium subsidy can bring that cost down dramatically, sometimes to a few hundred dollars a month or less. But the subsidy is entirely based on your household income as reported to the IRS, specifically your MAGI, your modified adjusted gross income. The lower your MAGI, the bigger the subsidy. The higher your MAGI, the smaller the subsidy or none at all.

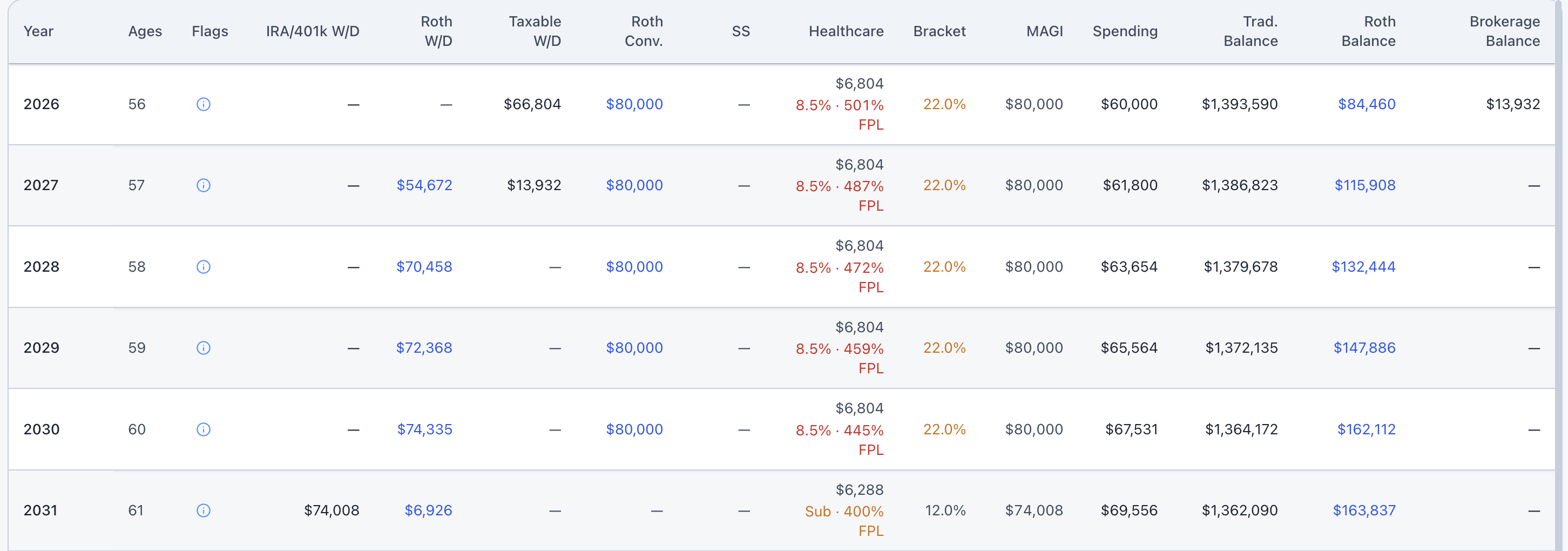

This is where the Roth conversion ladder runs into trouble, because every dollar you convert from a traditional IRA to Roth counts as ordinary income. The IRS treats a $70,000 conversion the same way it treats $70,000 in wages. That income pushes your MAGI up, and your subsidy goes down with it.

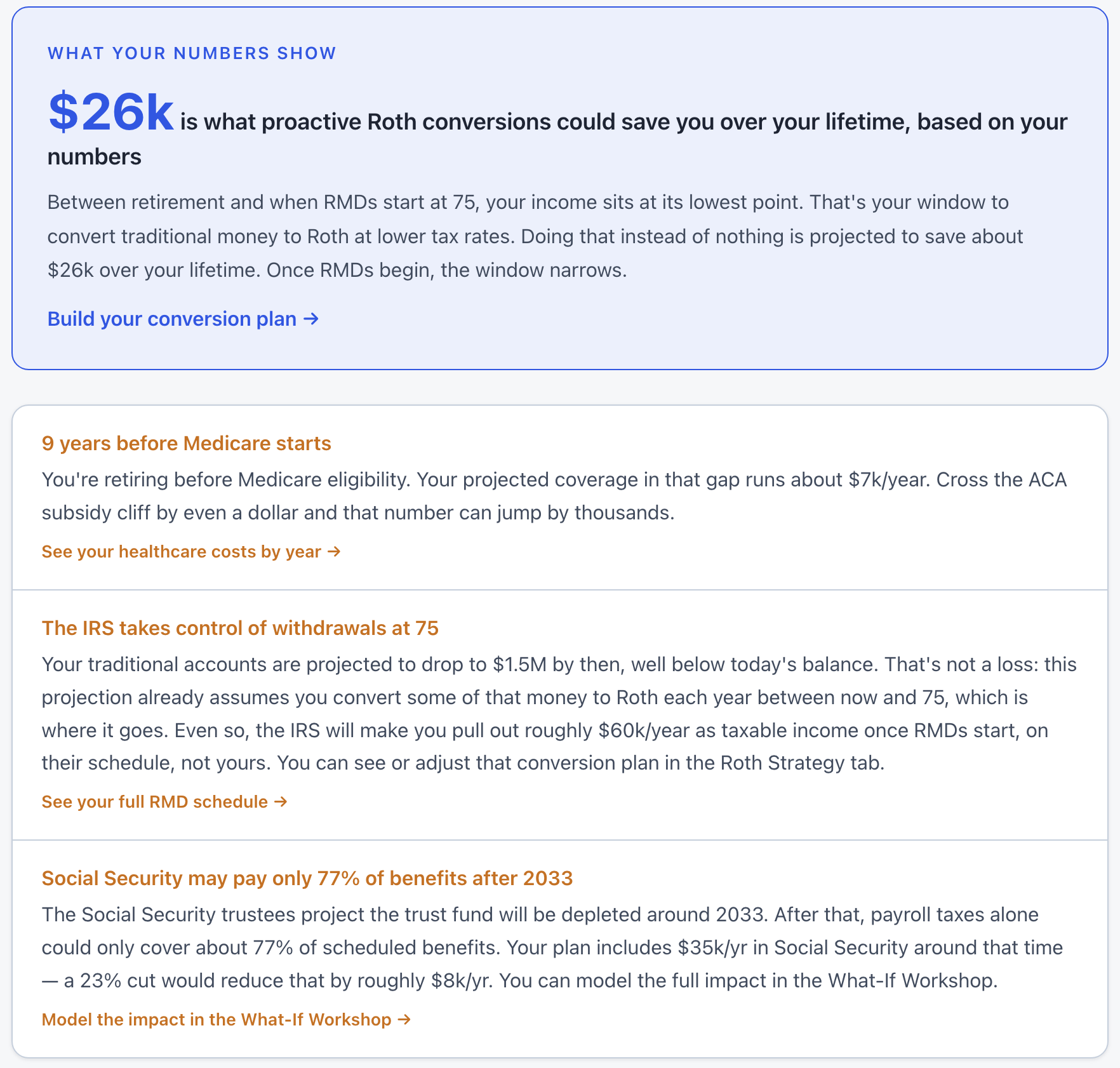

For someone retiring at 50, that exposure runs for 15 years. A ladder that costs you $12,000 per year in lost subsidies while you convert traditional money to Roth is a $180,000 problem on top of the income taxes you are already paying on the conversion itself. No ladder tutorial accounts for that number, because it requires modeling health insurance and retirement income together, not separately.

Why Brokerage Accounts Are the Secret Weapon for ACA Subsidies

Not all income counts the same way for ACA purposes. Wages, traditional IRA withdrawals, and Roth conversions all count as ordinary income and raise your MAGI directly. Long-term capital gains and qualified dividends from a taxable brokerage account also count toward MAGI, but they give you something the others do not: control.

When you live off a brokerage account in early retirement, you decide how much to realize each year. You can sell positions that have small gains. You can harvest losses to offset gains. You can time larger sales to years when you have more bracket room. In lower income years, long-term capital gains can be taxed at zero percent federally. None of that flexibility exists with traditional IRA withdrawals, which land as ordinary income regardless of how you structure things.

A retiree drawing $70,000 from a brokerage account in a year with mostly long-term gains might report $40,000 of MAGI after standard deduction considerations. The same person converting $70,000 from a traditional IRA for a Roth ladder reports $70,000 of ordinary income. The difference in ACA subsidy between those two outcomes can easily be $8,000 to $15,000 per year for a single person, and more for a couple.

This is why building a substantial brokerage account before retirement is so important for FIRE planning specifically. It is not just about having money accessible before 59 and a half. It is about having income that you can keep low on paper while still living well, which is what unlocks the ACA subsidy for potentially a decade or more.

The Two 5-Year Rules (And Why the Second One Is Overrated for Most FIRE Retirees)

The ladder is built around the second of two Roth 5-year rules, and they are not the same thing.

The first rule is about your Roth account itself. Before earnings can come out tax-free, your account must be at least five years old. This clock starts on January 1 of the first year you contributed to a Roth and never resets. If you have been doing backdoor Roth contributions since your thirties, this rule is almost certainly already satisfied.

The second rule is about conversions specifically. Each batch you convert from traditional to Roth starts its own five-year clock. If you withdraw that converted money before five years pass and you are under 59 and a half, you owe a 10 percent penalty. This is the rule the ladder is designed to work around.

Once you turn 59 and a half, the second rule disappears entirely. Someone retiring at 57 or 58 only needs to bridge a year or two to get past it. The ladder is solving an 11-year problem for someone who retires at 48, not a 2-year problem for someone who retires at 57. For the majority of FIRE retirees who retire in their mid to late fifties, the brokerage account handles the gap, the penalty window closes on its own, and no ladder was ever needed.

How the 3-Bucket Method Solves Both Problems at Once

The 3-bucket drawdown sequence is brokerage first, traditional second, Roth last. The order is not arbitrary. Each piece of the sequence is doing something specific.

Spending the brokerage account first keeps your MAGI low in the years before Medicare, which preserves ACA subsidies. It also bridges the gap to 59 and a half without touching your traditional accounts early, so no penalty applies. Once you pass 59 and a half, the traditional account opens up cleanly. You draw from that next, and because your income was low in the brokerage years, you may have room to do modest Roth conversions without blowing your subsidy, filling your bracket efficiently in the years between Medicare and RMDs at 73. The Roth account, which you built over your working years through backdoor contributions, sits untouched the entire time, compounding tax-free.

The ladder, by contrast, pulls from traditional accounts now and routes through Roth as a pipeline. It converts ordinary income today, pays tax on it today, raises MAGI today, and costs you subsidy dollars today, to solve a penalty problem that a big enough brokerage account would have solved for free. If your brokerage can cover you to 59 and a half, the ladder is solving the wrong problem.

Case Study: How a Roth Ladder Cost One Early Retiree Over $100,000

Kevin retires at 52 with $1.5 million in a traditional 401k and $280,000 in a taxable brokerage account. He has a Roth IRA with $120,000 in it, opened in his late thirties. He and his spouse plan to spend $80,000 per year.

Kevin reads about the Roth ladder and decides it makes sense. He converts $80,000 per year from his traditional 401k to Roth. He pays roughly $9,000 in federal income tax on each conversion. That part of the math looks fine.

What Kevin did not model is what that $80,000 conversion does to his ACA subsidy. As a couple with $80,000 in ordinary income, their MAGI puts them well above the range for meaningful subsidy. Their unsubsidized Silver plan costs $2,100 per month. Their subsidy effectively disappears. They pay $25,200 per year for health insurance.

Without the conversion, Kevin could draw $80,000 from his brokerage account, mostly as long-term capital gains. His MAGI lands around $55,000 after factoring in the gains and their standard deduction. At that income level they qualify for a substantial subsidy. The same Silver plan costs them $510 per month, or $6,120 per year.

The difference is $19,080 per year in health insurance costs. Kevin has 13 years until Medicare. The ladder saves him a 10 percent penalty on future withdrawals. But the ACA cost of running it comes to roughly $248,000 over those 13 years, on top of the income taxes he is paying on each conversion. The penalty he was trying to avoid over that same period on $80,000 per year would have been $104,000 total. The ladder costs him more than twice what the penalty would have.

The 3-bucket plan was a better answer. His brokerage covers him past 59 and a half with room left over. After that, his traditional account opens penalty-free. He does targeted Roth conversions in the Medicare window when health insurance is no longer tied to income. The Roth account he built through his working years stays untouched.

Case Study: When the Ladder Is Still the Right Answer

The ladder is not always wrong. Maria retires at 46 with $1.6 million in a traditional 401k, $90,000 in brokerage, and $80,000 in a Roth. She plans to spend $75,000 per year.

Her brokerage covers just over one year of spending. She has 13 and a half years until 59 and a half. The 3-bucket sequence cannot get her there without tapping her traditional account early, which means paying the 10 percent penalty. The ladder is genuinely her best path to avoid it.

But even here, the ACA math matters. Maria should not automatically convert her full spending need each year. She needs to calculate the subsidy she gives up with each additional dollar of conversion and weigh that against the penalty she avoids. In some years, converting $40,000 instead of $75,000 and accepting a small penalty on the remainder might still come out ahead of losing $12,000 in subsidies. The ladder is the right framework, but the conversion amount needs to be calibrated against the full cost, not just the tax bracket.

That calibration is exactly the kind of calculation that requires looking at taxes, penalties, and health insurance costs together. No one of those numbers tells the story on its own.

Why This Is So Hard to Plan Without the Right Tool

Most retirement calculators look at one thing at a time. A tax calculator tells you what you owe on a conversion. A penalty calculator tells you what you owe on an early withdrawal. A separate ACA calculator tells you your estimated subsidy. None of them talk to each other.

The problem is that these numbers are not independent. A conversion decision changes your tax bill, your ACA subsidy, and your future RMD exposure all at once. A brokerage withdrawal changes your capital gains tax, your MAGI, and your subsidy simultaneously. Optimizing any one of those numbers in isolation can make the others worse in ways that cost far more than you saved.

This is what ThunderHarbor was built to do. The planner models your three buckets together, shows you how each withdrawal decision affects your MAGI and your ACA subsidy in real time, and lets you see the true cost of a Roth ladder versus the 3-bucket sequence for your specific numbers and your specific retirement date. The result is often the opposite of what a standard calculator suggests, because the standard calculator was only looking at part of the picture.

The Honest Summary

The Roth conversion ladder is a real strategy. It solves a real penalty problem for a specific type of early retiree: someone retiring well before 59 and a half with very little in a taxable brokerage. If that is your situation, the ladder belongs in your plan, but the conversion amounts still need to be sized against what you lose in ACA subsidies each year.

For most FIRE retirees who retire in their mid to late fifties with a meaningful brokerage account alongside their traditional and Roth savings, the 3-bucket sequence handles the bridge problem without the ladder mechanics, keeps MAGI low enough to preserve health insurance subsidies for a decade or more, and leaves the Roth compounding untouched for as long as possible.

The ladder tutorial focuses on one number: the 10 percent early withdrawal penalty. A complete retirement plan has to look at all of them together.

Not financial advice

This article is for informational purposes only. Nothing here constitutes financial, tax, or legal advice. ACA subsidy rules and tax brackets change from year to year. Always consult a qualified professional before making significant financial decisions.

See what the ladder actually costs in your situation

ThunderHarbor models your brokerage, traditional, and Roth accounts alongside your ACA subsidy so you can compare strategies with the full cost in view, not just the tax bill.

Start your free plan