June 10, 2026

Retirement Means Running Your Own Company. RMDs Are Just One Line Item

Mark retired at 52. The first few months were everything he pictured: slow mornings, a woodworking project he had put off for a decade, a trip to visit his daughter without checking his email once. Around month four, he sat down to reconcile his accounts for the quarter and realized something. He was not retired from work. He had just been promoted, with no warning, into running a small company that owned his entire financial life. And nobody had handed him an org chart.

The departments that used to belong to someone else

For thirty years, Mark worked as an operations manager at a mid-size manufacturer. Payroll withheld his taxes. HR managed his health plan and his 401k enrollment. Legal made sure the company filed what it needed to file. Mark showed up, did good work, and let the rest of it run in the background. He never thought about it because he never had to.

The day he retired, every one of those departments closed and reopened with him as the only employee. He is now the CFO who builds the budget, the HR department that manages his own health insurance, and the legal team that tracks the deadlines the IRS and Medicare set for him. Nothing about his money changed overnight. What changed is that nobody else is watching it anymore.

CFO: the budget has two halves, and Mark only saw one

Mark built a spending plan before he retired. Groceries, utilities, insurance, the usual monthly bills. It came to about $5,800 a month, $69,600 a year, and his investments could comfortably support that. On paper, he looked solid.

What his plan did not include was the other half of the budget. His roof was 19 years old and would need replacing within five years, around $16,000. His car was nine years old and would likely need replacing within three, call it $32,000. His HVAC system was original to the house. None of these are surprises. They are predictable costs that simply do not happen every month, so they are easy to leave off a monthly budget entirely.

A real company calls this the difference between operating expenses and capital expenses. Mark’s monthly number was his opex. The roof, the car, and the HVAC system are his capex, and they were due to land in years two, three, and six of his retirement. If any of those years also happens to be a year where a large withdrawal would push him over an ACA subsidy cliff, the timing of a $32,000 car purchase suddenly matters a great deal.

Legal: the deadline that was set the day he retired, due in 23 years

Mark has $450,000 in a traditional 401k that he rolled into an IRA. He is not touching it. His brokerage account and Roth cover his spending until Social Security starts. The 401k just sits there, growing.

Mark was born in 1974, so his Required Minimum Distributions begin at 75, in 2049. That is 23 years away. Grow $450,000 at a modest 6% a year for 23 years and it becomes roughly $1.72 million. The IRS divisor at 75 is 24.6, which makes his first RMD about $70,000 in a single year. That is almost exactly what Mark spends in a year today, except this $70,000 arrives as fully taxable income whether he needs it or not, on top of Social Security, in the same year the IRS also starts looking at his tax return from two years earlier to set his Medicare premium.

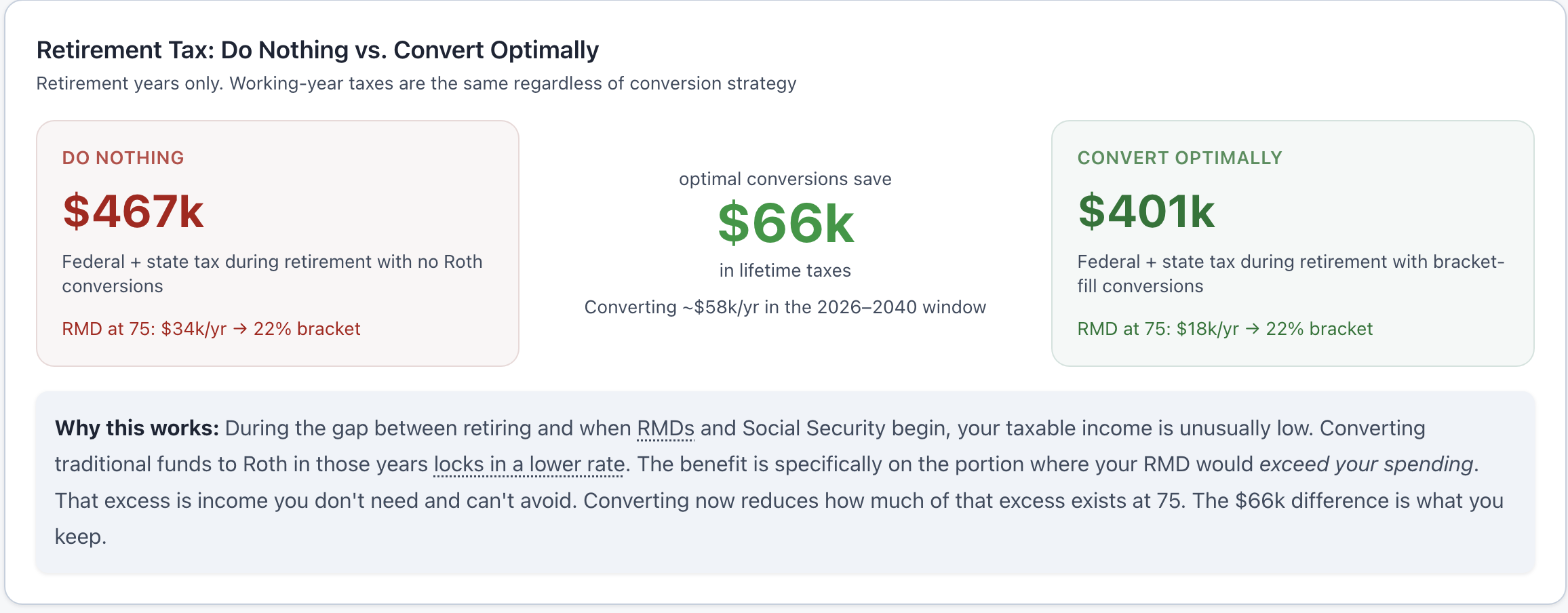

Nothing about this is unusual or a sign Mark did anything wrong. It is what happens to any balance left untouched for 23 years. The reason it is worth knowing about now, at 52, is that the next 13 years before Social Security starts are the cheapest years Mark will ever have to deal with it. His income in those years is lower than at any other point in his life. Converting a portion of that 401k to a Roth IRA each year, just enough to stay under the next tax bracket or the ACA subsidy cliff, would shrink that $1.72 million number steadily, before the IRS schedule forces the issue. The strategy is not complicated. The only hard part is that the deadline is 23 years out, and 23 years is a very easy thing to not think about.

Treasury: Social Security and the RMD share a tax return

Mark has not decided when to claim Social Security. At 67 he would get about $2,400 a month, $28,800 a year. At 70 it would be closer to $3,570 a month, $42,800 a year. The common advice is to wait if you can afford to, and for most people that is right. But Mark will be 75 in the year his RMDs also start, which means whatever Social Security decision he makes now will be sitting on the same tax return as that $70,000 forced withdrawal, decades from now.

Up to 85% of Social Security becomes taxable once combined income crosses certain thresholds. A $70,000 RMD on top of $42,800 of Social Security would put nearly all of that Social Security into the taxable column, on top of pushing Mark into a higher bracket than he is in right now, working full time. Treasury and legal are not two separate conversations for Mark. They are the same spreadsheet, just years apart.

The good news and the catch

Once Mark saw all of this laid out, his reaction was not dread. It was closer to relief. For the first time, he could see the whole picture instead of just the monthly number. He could decide, on his own terms, to convert some of his 401k each year while his income is low. He could plan the car purchase for a year when a bigger withdrawal would not cost him an ACA subsidy. Nobody at his old company ever gave him this kind of visibility into his own money.

The catch is that the visibility only helps if someone keeps looking. Mark’s old HR department sent reminder emails about open enrollment. Nobody is going to send Mark a reminder in 2049 that says his RMDs are starting, except in the form of a tax bill. The company runs fine as long as the owner keeps showing up to run it.

What the app models

ThunderHarbor is the back office Mark did not have. It projects his 401k balance all the way to 75 based on his actual birth year, and shows the dollar size of that first RMD next to his projected Social Security and tax brackets in that same year, decades before either one arrives. It lets him add the roof, the car, and the HVAC system as one-time expenses in the specific years he expects them, and shows what those withdrawals do to his ACA subsidy or tax bracket in that year, not just his average.

From there, Mark can test a Roth conversion amount for each of the next 13 years and watch the projected RMD shrink in response. The same projection that surfaced the $70,000 problem decades early is the one that shows him whether this year’s conversion is actually moving the number.

The honest bottom line

Mark did not need to spend his first year of retirement worrying about a tax bill due in 2049. But he also could not afford to forget it existed. RMDs, Social Security, the roof, the car, the health plan: none of these are separate problems that show up one at a time on a schedule. They are departments in the same small company, and as of his retirement date, Mark is the only one running all of them. The people who handle this well are not the ones who panic the year the first RMD arrives. They are the ones who, sometime in that first year, realized they had been promoted and decided to actually do the job.

Not financial advice

This article is for informational purposes only. Nothing here constitutes financial, tax, or legal advice. Always consult a qualified professional before making significant financial decisions.

See your whole company on one page

ThunderHarbor projects your RMDs, Social Security, taxes, and big one-time expenses together, year by year, so nothing slips through because no one was watching.

Start your free plan