June 5, 2026

The Pension Retirement Tax Trap: What Your Employer Never Told You

If you have spent a career in a job that comes with a pension, you probably feel pretty good about retirement. You have a guaranteed monthly check coming in for life. You did not have to stress about the stock market the way your friends at private companies did. That security is real, and you earned it. But there is a tax planning problem hiding inside that sense of security that catches pension holders off guard more than almost any other group, and it starts long before the IRS gets involved.

The assumption that creates the problem

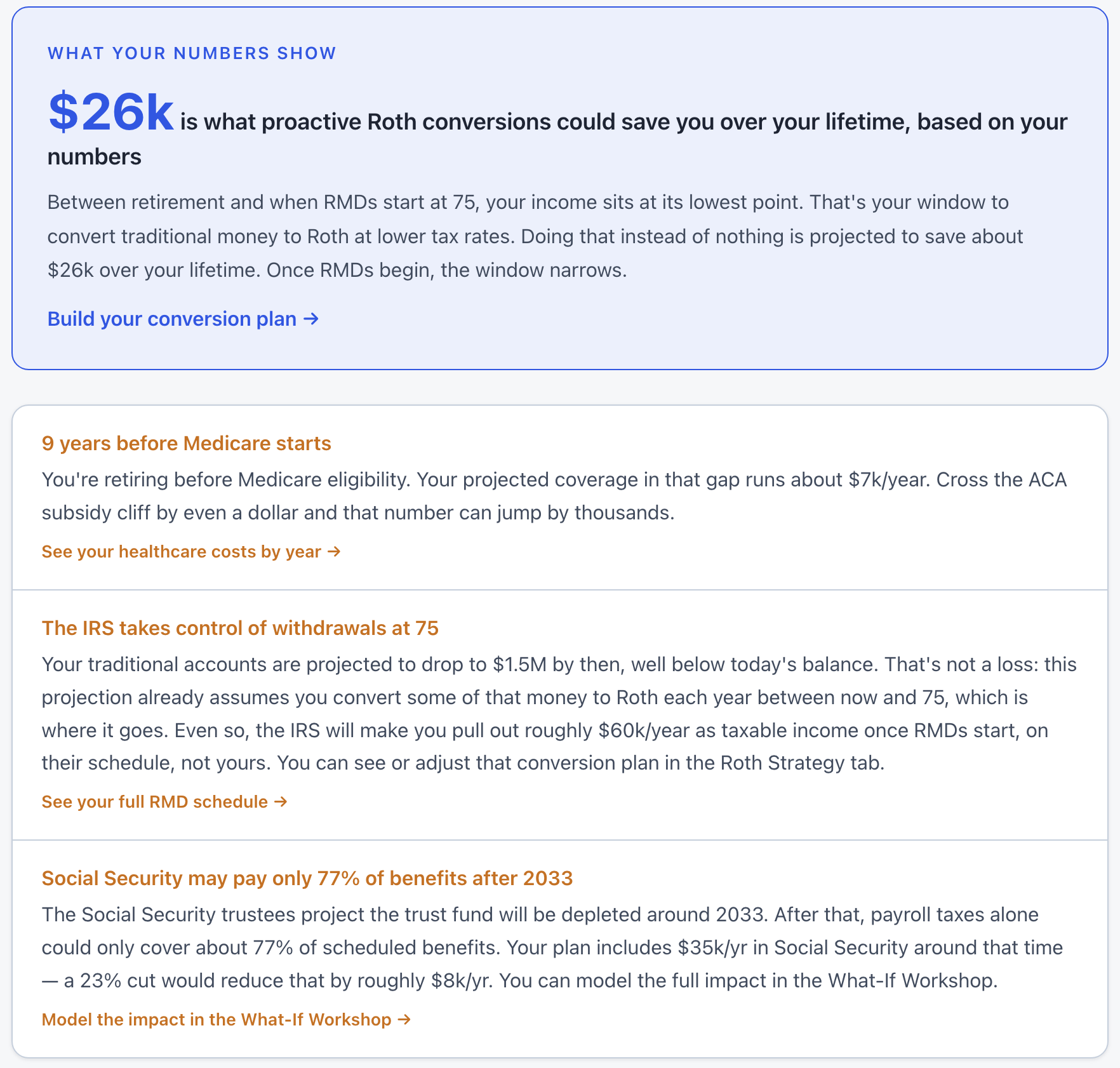

Pension holders tend to leave their traditional IRA or 401k completely untouched in retirement. The pension covers the bills, so there is no urgent reason to touch the IRA. That logic is understandable. You spent decades building that balance, and it feels good to watch it keep growing. But the IRS does not care whether you need the money. Once you turn 73, they require you to start withdrawing from traditional accounts on their schedule, not yours. Those Required Minimum Distributions are calculated from your total balance, and after a decade of sitting untouched, your IRA has likely grown considerably.

The result is an income stack that nobody warned you about. Pension income. Social Security. Forced IRA withdrawals. All three land in the same year, all three count as taxable income, and the total can push you into a bracket that is higher than anything you saw during your working years. The pension feels like security. In practice, it becomes a fixed floor that makes every other income source more expensive.

The healthcare problem that comes first

Before RMDs even enter the picture, many pension holders face a different income problem: health insurance. Not every pension comes with retiree medical coverage. Teachers, government workers, and private sector employees with pension plans often retire in their late fifties or early sixties, well before Medicare begins at 65. That means buying health insurance on the ACA marketplace for several years.

ACA subsidies are income-based, and the pension counts. The subsidy cliff sits at 400% of the federal poverty level. For a single person in 2025, that is roughly $60,000 in modified adjusted gross income. Cross it by a dollar and you lose the entire subsidy. Full market rate for a comprehensive plan can easily cost $1,000 or more per month. If your pension already puts you near that threshold, any IRA withdrawal for living expenses can push you over, and the subsidy disappears entirely. You now need to pull even more from the IRA just to cover the higher insurance cost, which pushes your MAGI higher still.

Meet Dave: a real scenario

Dave is 62, single, and just retired from a manufacturing company that offered a pension. His pension pays $50,000 a year. He also has a traditional IRA with $300,000 that he has never touched. His employer did not offer retiree health coverage. He expects Social Security at 67, roughly $22,000 a year.

Dave’s spending runs about $68,000 a year. His pension covers most of it, so he takes about $18,000 from the IRA to close the gap. His MAGI lands at $68,000. That is above the ACA subsidy cliff. He pays full market rate for his health plan, about $900 a month, which adds another $10,800 a year. Now he needs $28,800 from the IRA to break even. His MAGI climbs to $78,800. Social Security becomes 85% taxable once income crosses $34,000 for a single filer, so when SS begins at 67, almost all of it will be taxed. By the time RMDs start at 73, his IRA has been growing quietly in the background. A $300,000 balance growing at 5% over eleven years becomes roughly $515,000. His first RMD is around $19,000. Stacked on pension plus Social Security, his total income is near $91,000. He is firmly in the 22% bracket and approaching Medicare IRMAA territory.

Dave did nothing wrong. He saved diligently, collected his pension, and spent carefully. But because nobody told him to plan for the income stacking problem, he is now paying taxes and healthcare premiums on money he did not choose to receive.

The window that most pension holders ignore

Between the day you retire and the day Social Security starts is often the best tax planning window of your entire life. Your income is lower than it will ever be again. Pension only, no SS, no RMDs. For many people that is a window of five to ten years where strategic Roth conversions are cheaper than at any other point.

A Roth conversion moves money from your traditional IRA to a Roth IRA. You pay ordinary income tax on the amount you convert in that year. In exchange, that money grows tax-free and is never subject to RMDs. The goal is not to convert everything at once. It is to convert enough each year to keep your total MAGI below the ACA cliff and below the next tax bracket threshold, gradually shrinking the traditional IRA balance before forced distributions make the decision for you.

For Dave, his pension is $50,000. The ACA subsidy cliff for a single person is around $60,000. That leaves roughly $10,000 of room per year to convert without losing his subsidy. Over five years before Medicare starts, he can move $50,000 to Roth, paying tax at a modest rate. At 65, Medicare removes the ACA concern. He now has more room and can accelerate conversions through his late sixties before SS begins at 67. Even a modest conversion pace materially reduces the IRA balance that will eventually become RMDs.

When conversion is not optional

Not every pension holder has the luxury of choosing whether to do Roth conversions. If your pension and spending are tightly matched and you need to pull from the IRA just to cover basic living expenses, conversion takes a back seat to survival. Paying the bills comes first. The planning question in that case shifts from “how much should I convert” to “what is the most tax-efficient way to take the withdrawals I already need.”

Even then, the timing matters. If you know you will need $20,000 from the IRA in a given year, taking it in one large distribution versus spreading it across two tax years can change your bracket. A withdrawal that lands inside the 12% bracket has a very different cost than one that spills into 22%. The calendar is a tool that most people forget to use.

The income you actually keep

Here is the part of the picture that surprises people most. Once you add up what actually reaches your bank account after taxes, healthcare, and any Medicare premiums, the effective income from a pension can feel much smaller than the headline number. Pension income is fully taxable as ordinary income in most states. Social Security is up to 85% taxable federally once your combined income crosses the relevant threshold. IRA withdrawals add on top of that. If you are in the IRMAA surcharge zone, your Medicare Part B premium can easily double or triple from the standard amount.

The net result is that a pension that looks like $50,000 a year can deliver meaningfully less than that in actual spending power once taxes, insurance, and healthcare surcharges are factored in. That gap is what planning is supposed to close. Not by avoiding taxes entirely, but by structuring income so the government takes the smallest legal share.

What the app models

ThunderHarbor is built to handle exactly this type of scenario. You enter your pension amount, start age, and whether it includes a cost-of-living adjustment. The projection engine combines that with your Social Security estimate, any IRA or 401k balances, and your spending target. Every year of the projection shows your actual MAGI, where it sits against the ACA subsidy cliff and IRMAA thresholds, and what your tax bill looks like with and without planned Roth conversions.

If you have a spouse with a separate pension, that income stacks as well. Survivor benefits are modeled so you can see what happens to the household income picture if one partner dies. The Tax Cliffs tab shows every year flagged red, orange, or yellow depending on how close your projected income lands to each major threshold. If you are close to the ACA cliff before 65 or approaching IRMAA territory in your seventies, the app surfaces that before it happens, not after.

The honest bottom line

A pension is a genuinely valuable thing. The predictability alone is worth a great deal when markets are volatile. But guaranteed income is not the same as tax-efficient income, and the two are different problems. The people who come out ahead are the ones who treat the pension as a starting point for the plan, not the end of it. The window to act is real and it closes faster than most people expect. Once RMDs start and Social Security is locked in, your options narrow considerably. The earlier you model what the income stack actually looks like, the more room you have to do something about it.

Not financial advice

This article is for informational purposes only. Nothing here constitutes financial, tax, or legal advice. Always consult a qualified professional before making significant financial decisions.

See your pension income stacked against every tax cliff

ThunderHarbor projects your pension, Social Security, IRA withdrawals, and RMDs year by year, and shows exactly where your income lands against the ACA cliff, IRMAA thresholds, and tax brackets.

Start your free plan